Author: Oluwapelumi Adejumo, Cryptoslate

Compiled by: Deep Tide TechFlow

Introduction: Trading volume hasn't collapsed, but active addresses have been shrinking for six consecutive months, falling to a five-year low. This divergence between "superficial prosperity and internal emptiness" is a negative signal of the structural health of the bull market.

The article uses three sets of data—Glassnode, Santiment, and CryptoQuant—for cross-validation and proposes three future scenarios, providing a suitable reference framework for judging the current trend of BTC.

The full text is as follows:

Bitcoin's network activity has weakened for six consecutive months, but this trend is not reflected in the core metrics that many traders look at first glance.

The clearer signal isn't transaction volume—which has remained largely stable—but rather the breadth of participation. Even as the network continues to process a similar number of transactions, the number of active on-chain addresses is steadily declining.

This divergence is crucial in a market where price discovery increasingly occurs in ETFs and derivatives. It means that Bitcoin's on-chain footprint is narrowing, while its market exposure continues to be active elsewhere.

As the bear market continues, this trend has become increasingly difficult to ignore.

According to Glassnode data, in mid-August 2025, the eight-day average of active Bitcoin addresses was approximately 778,680. As of February 23, this number had dropped to approximately 535,942, a decrease of about 31%.

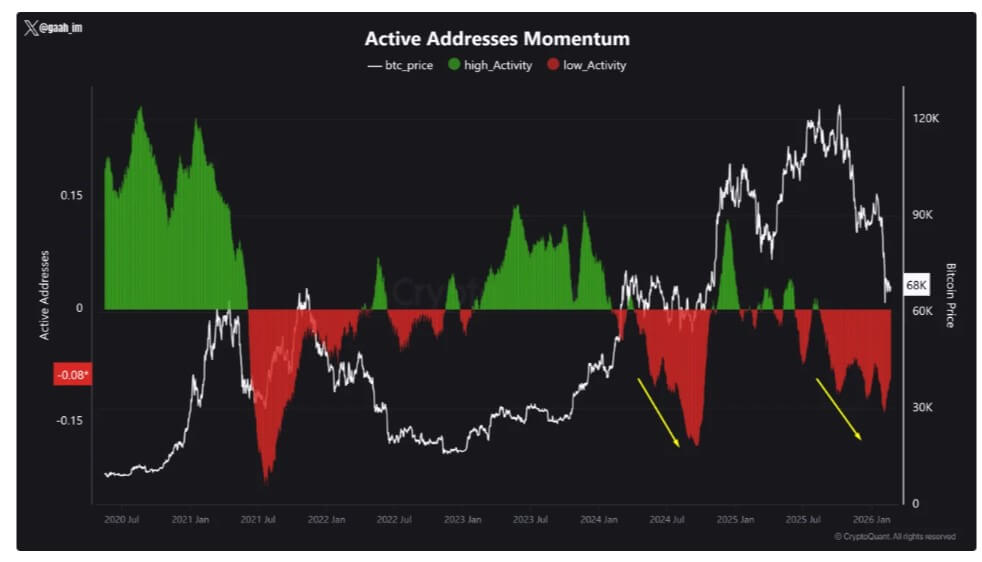

CryptoQuant has also flagged low network activity for six consecutive months, describing the current phase as a period of continued weakness in on-chain engagement.

Bitcoin Active Addresses Momentum, Source: CryptoQuant

The last time the market exhibited a similar pattern was in 2024—Bitcoin subsequently experienced a pullback of approximately 30%.

This doesn't mean it will definitely happen again now, but it reinforces a historical pattern: prolonged network weakness often coincides with periods of weakening market confidence.

The breadth of reach declined, but the throughput did not collapse.

The number of Bitcoin transactions did not decrease in tandem with the number of active addresses.

In mid-August 2025, the average daily number of transactions was approximately 444,000. Data from Blockchain.com shows that the average daily number of transactions over the past 30 days was approximately 439,000.

The daily data still fluctuated, ranging from approximately 289,000 to 702,000 transactions, but the overall throughput trend did not collapse.

This divergence is key to understanding the current situation.

If transaction volume remains stable while active addresses decrease, it indicates that fewer entities are undertaking the same amount of on-chain activity.

There are several reasons for this situation, none of which require an influx of retail investors. Exchanges and custodians can process withdrawals in bulk; large investors can consolidate transfers; institutional funds can be processed with fewer wallets; operational activities may also cause a temporary surge in the number of transactions, but this does not represent a genuine return of users.

The result is that while the blockchain still appears busy, the number of participants at the underlying level is decreasing.

This is why a decline in breadth is more telling than raw throughput. A flat number of trades may mask a market where activity is increasingly concentrated among repeat traders, large institutions, and operational cash flows.

In this scenario, the Bitcoin blockchain still functions normally, but the breadth of user participation it represents is no longer as genuine.

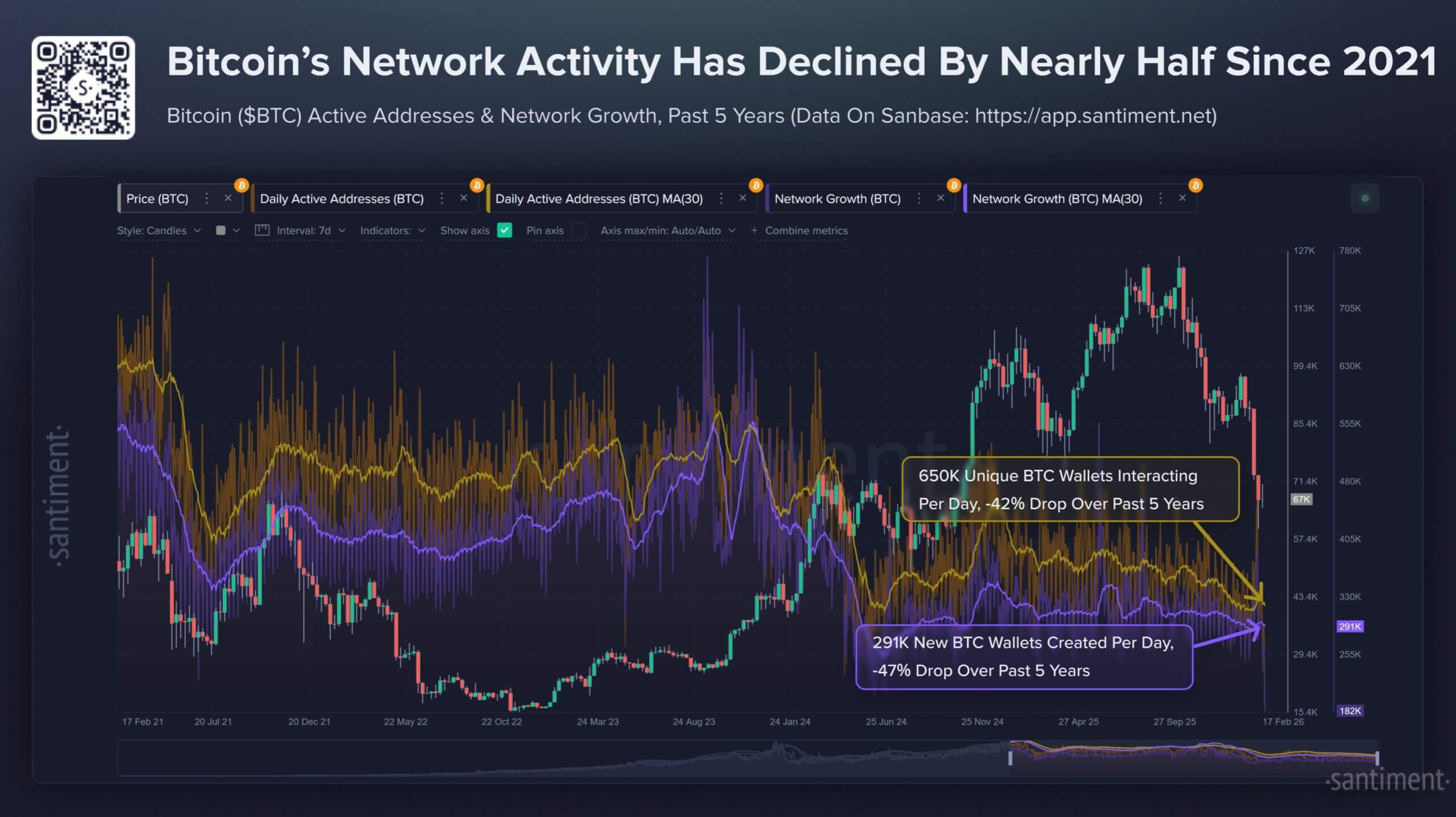

Blockchain analytics firm Santiment offers a more straightforward description from a longer time horizon.

The agency stated that since February 2021, the number of unique addresses initiating Bitcoin transactions has decreased by 42%, and the number of newly created addresses has decreased by 47%.

Santiment did not characterize this as evidence that crypto is dead or that a multi-year bear market has been locked in, but it did describe a bearish divergence throughout 2025—market capitalization is rising while Bitcoin's utility metrics are weakening.

This tension is now reflected in the six-month trend. Prices and market narratives may continue, but the chain itself is becoming increasingly quiet.

Low transaction fees indicate shrinking demand for blockchain space.

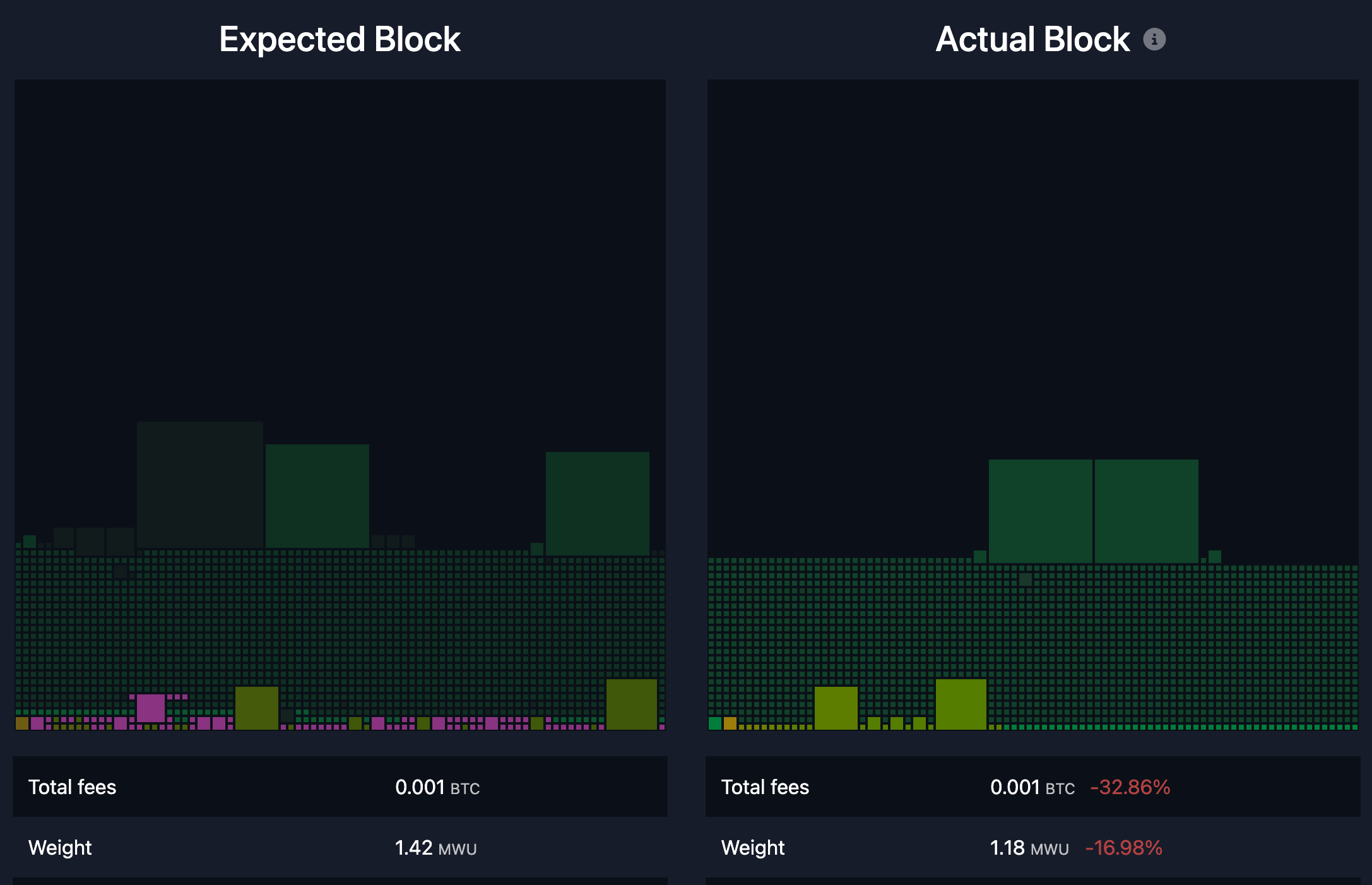

The transaction fee data further confirms that Bitcoin Layer 1 is experiencing weak demand.

Data from mempool.space shows that the network's recent average transaction fee is approximately $0.24, or about 1.8 sats/vB.

This is a low level for a network that has experienced sustained competition for block space during past cycle peaks. Based on the current transaction pace, this fee level means the network's daily fee revenue is less than $100,000.

In contrast, block subsidies are currently around 450 BTC per day, representing a very small percentage of transaction fee revenue.

Bitcoin Average Block Fees, Source: Mempool.space

This is not an immediate security issue, nor does it mean that Bitcoin's security model is facing any immediate pressure.

This is because block subsidies still dominate miners' revenue. But it does point to a long-term reality that Bitcoin has not yet been forced to confront at this stage of this cycle.

The topic of transitioning to a cost-supported security budget comes up every cycle, but in the current environment, this transition has not been tested—because the demand for fees is weak to begin with.

In reality, the current quiet transaction fee market has further delayed this discussion.

The chain is not facing persistent congestion pressure, and users are not fiercely bidding to get on board. This situation could change rapidly in the event of volatility, speculative waves, or new demand shocks, but that hasn't happened yet.

Currently, the use of blockchain space is significantly lower than in previous bull market phases, which is consistent with the overall decline in participation.

Bitcoin's Empty Mempool, Source: Mononaut

CryptoQuant's assessment aligns with this fee environment—low network activity is typically associated with declining market interest in assets and periods of widespread losses.

As interest wanes, new participants decrease, and self-initiated transfers decrease, the pressure of transaction fees diminishes.

Bitcoin remains actively traded as a financial asset, but the blockchain itself no longer reflects widespread user participation.

Macroeconomic conditions and ETF fund flows are changing the way Bitcoin is traded.

The macroeconomic context helps explain why this trend persists.

Bitcoin is increasingly resembling a high-beta asset that is sensitive to macroeconomic conditions, especially during periods of risk aversion.

Over the past year, US inflation has cooled somewhat, with the CPI year-on-year growth rate in January 2026 at 2.4%; the Federal Reserve's target interest rate range was cited as 3.50% to 3.75% at the end of January.

In a simpler market environment, cooling inflation may support a clearer rebound in risk assets.

However, market attention is focused on several catalysts for volatility, including uncertainty surrounding tariff policy. This factor has driven sharp fluctuations in interest rates and the US dollar, keeping overall risk appetite volatile.

In this environment, both retail and institutional investors tend to reduce their trading frequency. Retail participation decreases, and trader turnover decreases. Institutions can maintain exposure, but are more inclined to adjust their positions through products that do not require on-chain transfers.

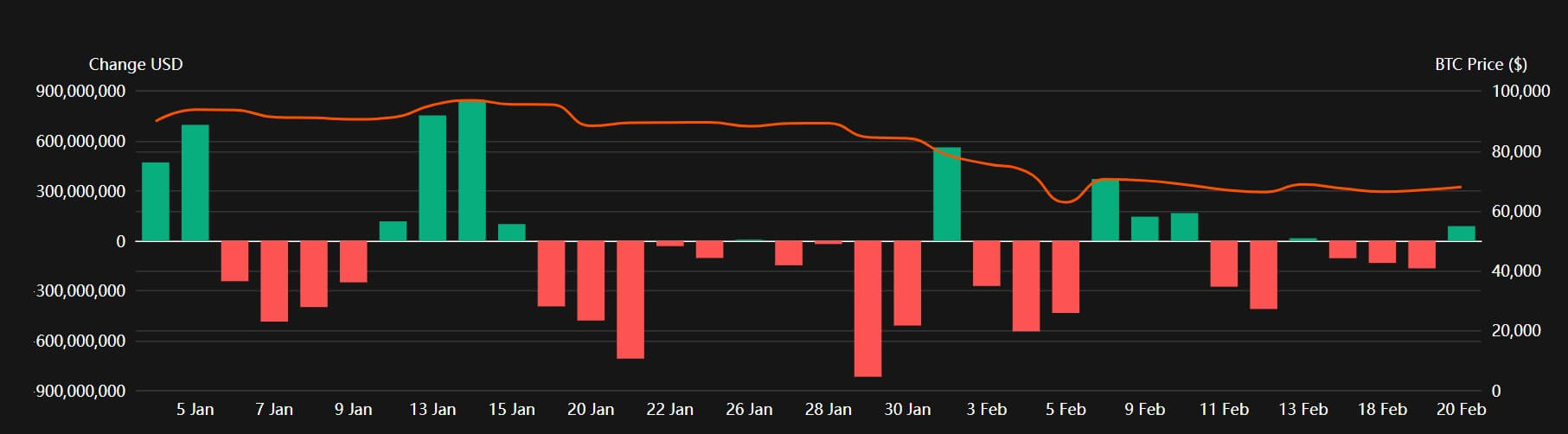

This is precisely why spot Bitcoin ETFs have become key protagonists in the narrative.

According to Coinperps data, US Bitcoin ETFs have seen net outflows for several consecutive weeks, with a cumulative outflow of approximately $3.8 billion in the past five weeks and approximately $4.5 billion year-to-date.

Daily fund flows of US Bitcoin ETFs in 2026, Source: Coinperps

This moved the activity from the self-custodied wallet to the brokerage account.

This also explains why the market can remain active, while the blockchain is becoming increasingly quiet. While open positions are still changing hands, more transactions are taking place off-chain.

This represents a significant shift in Bitcoin's role. It is increasingly resembling a financial product with an institutional shell, while Layer 1 is being used more selectively for settlement, storage, and periodic transfers.

Meanwhile, the daily trading energy in the crypto space is concentrating on other areas, especially stablecoins.

Coin Metrics lists stablecoins as a core driver of on-chain activity, with the total supply of stablecoins currently approaching $300 billion and trading volume continuing to climb.

If other on-chain stablecoin tracks take on more daily settlement needs, Bitcoin's Layer 1 will naturally become more functionally singular.

This in itself does not weaken the investment logic of Bitcoin, but it does change its form.

Three scenarios for the next three to six months

The current six-month decline in network breadth has created three possible paths for Bitcoin's future trajectory.

The first scenario is continued indifference , which appears to be the baseline scenario in a risk-averse market environment.

In this scenario, active addresses remain low (between 450,000 and 600,000), the number of transactions fluctuates but does not collapse, transaction fees remain low, and ETF fund flows remain stable or slightly negative.

Here, Bitcoin may still fluctuate wildly due to macro headlines, but on-chain participation does not confirm a broad recovery. The trading logic of the asset is more like a macro tool than a network entering a new phase of expansion.

The second option is to thaw the liquidity , which is a more optimistic path.

If inflation continues to cool and easing expectations stabilize risk appetite, ETF fund flows may shift from net outflows to sustained net inflows. In this environment, the growth in active addresses will be a key confirmation signal.

A rebound to 650,000 to 800,000 active addresses would indicate a recovery in engagement breadth, not just a return of price momentum. This looks more like a classic cyclical recovery – price increases supported by increased on-chain user engagement.

The third scenario is structural substitution , which is perhaps the most noteworthy.

In this scenario, Bitcoin prices rise, but on-chain breadth remains low. ETFs, derivatives, and custodial settlements continue to dominate, while stablecoins are absorbing more transaction demand elsewhere in the crypto space.

Here, Bitcoin is increasingly resembling a digital macro asset and settlement layer, rather than a chain with widespread daily retail activity.

This scenario would mark the evolution of Bitcoin's role, reflecting the profound changes it has undergone compared to many years ago.

{kind=link}