Authors: 21Shares Research Team

Compiled by: Deep Tide TechFlow

Deep Dive: 21Shares research team released an in-depth report on Hyperliquid, with the core argument being that Hyperliquid has evolved from a crypto derivatives DEX into a 24/7 full-service exchange. During the Iranian airstrikes in February, when the CME was closed, WTI crude oil contracts on Hyperliquid were priced nearly 48 hours ahead of schedule. Traditional asset trading volume now accounts for 35%, revenue is approaching that of the CME, but its valuation multiple is only half that of the latter. This report provides valuations under both bull and bear market scenarios and is worth reading carefully.

On February 28, the US-Israeli coalition launched airstrikes against Iran, plunging traditional markets into darkness. The Chicago Mercantile Exchange (CME) closed, its traditional infrastructure unable to respond. Hyperliquid, however, remained operational. This blockchain-based derivatives exchange ran 24/7, with WTI crude oil perpetual contracts priced in real-time, surging to $111.53, while traders in traditional markets could only watch helplessly.

This event highlights Hyperliquid's role as a key trading venue and index during periods of heightened geopolitical tensions—providing real-time price discovery during the weekend gap. When traditional markets reopened on March 2nd, WTI had pushed above $110, and the spread between Hyperliquid and CME had been closed. Hyperliquid didn't just react faster; it essentially priced in the shock nearly 48 hours earlier than traditional systems.

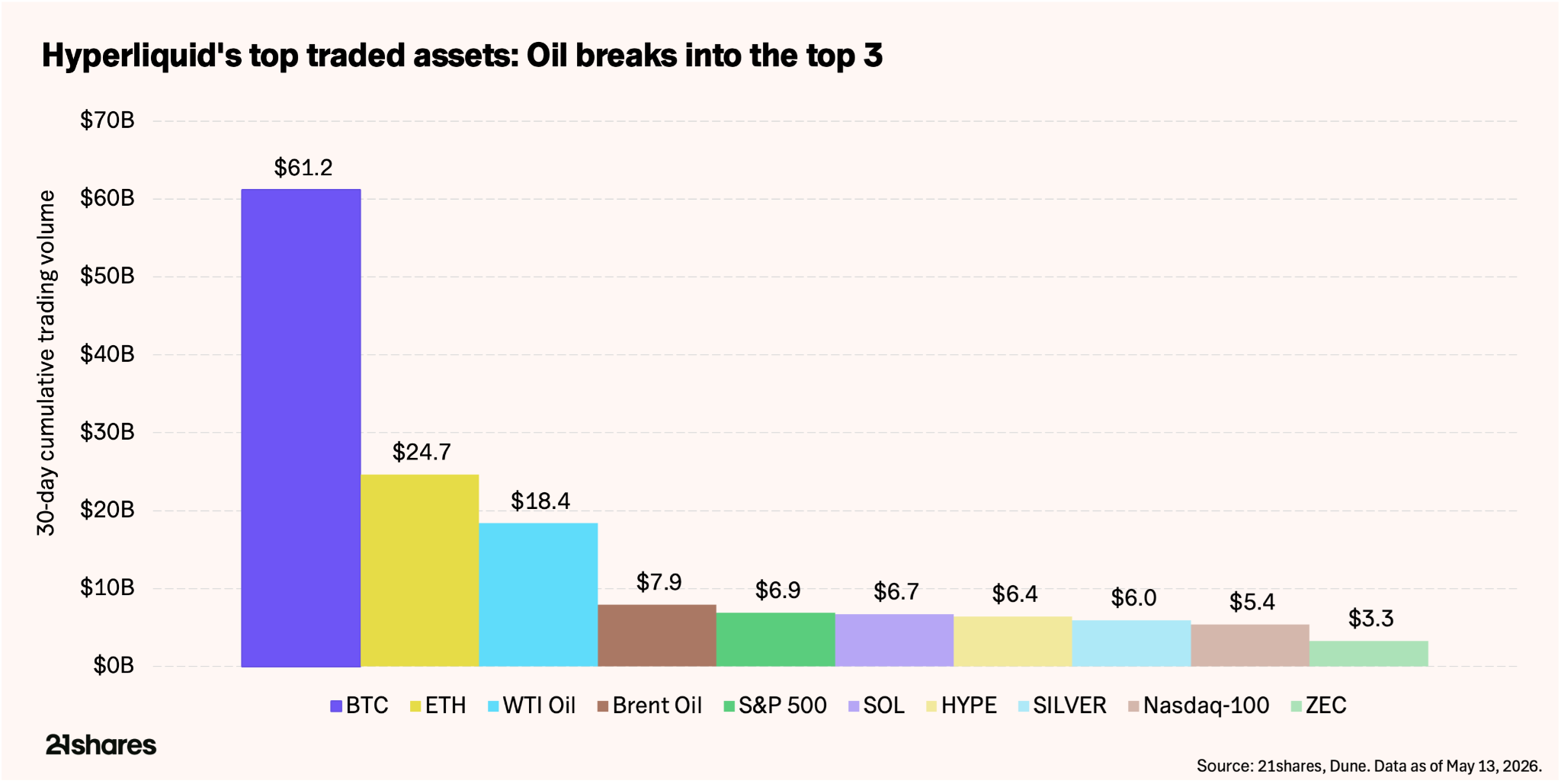

The narrative itself was convincing enough. But what turned it into an investment story was what happened later. Fast forward two months, and crude oil still had a 24-hour trading volume of about $500 million on Hyperliquid, making crude oil contracts one of the top five most traded assets on the platform.

Bitcoin remains the most traded asset on Hyperliquid, but traditional assets—S&P 500, silver, Nasdaq 100, WTI, and Brent crude oil—occupy half of the top ten most traded assets. Individual stocks like Micron Technology (MU) have even managed to squeeze into the top ten on some days. We believe this demonstrates Hyperliquid's ultimate direction. Hyperliquid is no longer just an exchange for trading crypto perpetual contracts; it has become a true "exchange for everything," where users can trade perpetual contracts for virtually any type of asset.

Caption: Distribution of the top ten traded assets on the Hyperliquid platform

Hyperliquid's business model is evolving.

This report will help you understand how to reasonably value Hyperliquid, and what key metrics and risks investors should monitor.

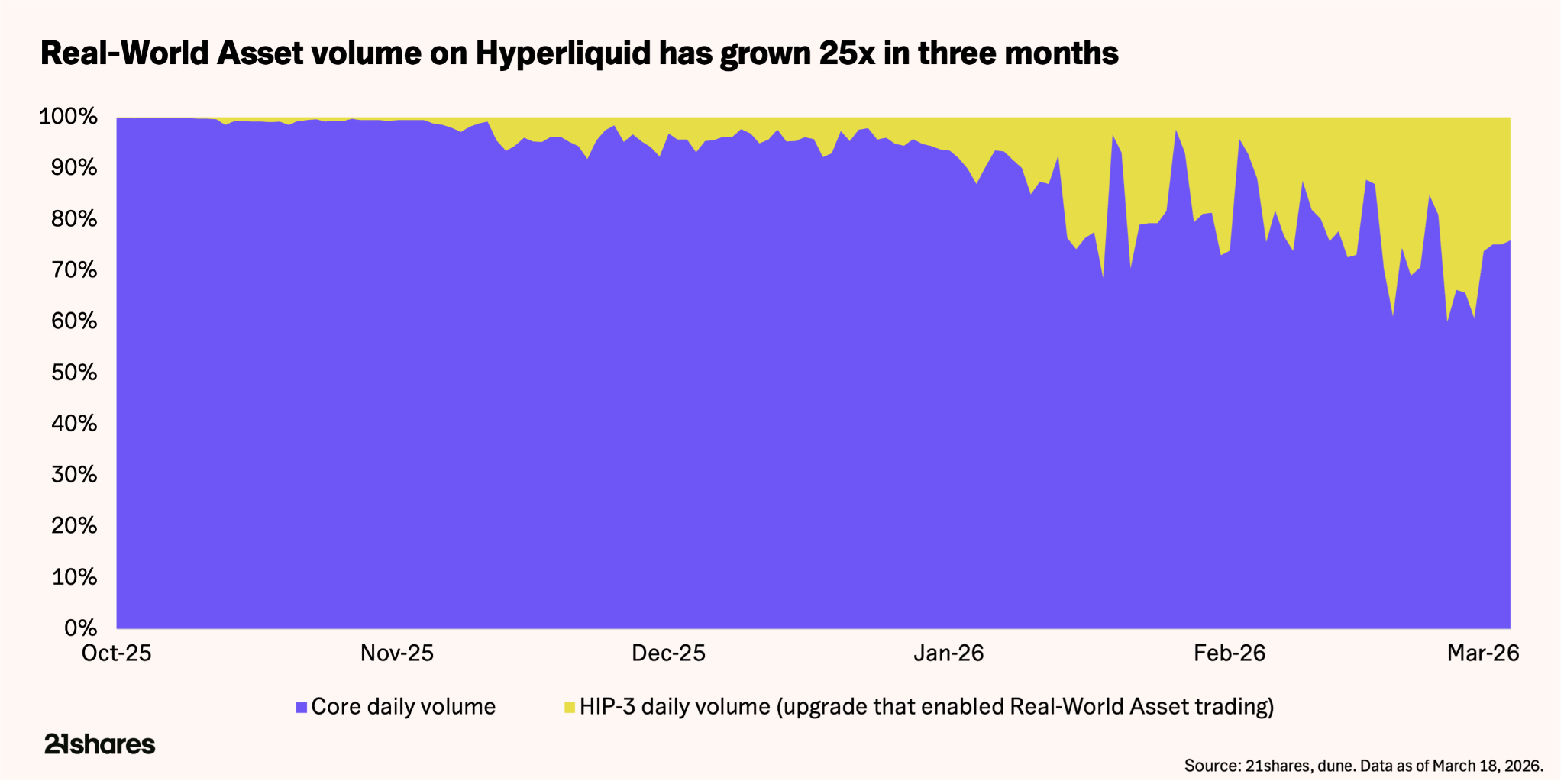

In the past, Hyperliquid derives most of its revenue from digital asset trading, and its business model is highly correlated with the overall trend of the crypto market. However, the growth in non-digital asset trading volume has fundamentally broadened the platform's core business model.

HIP-3 is a permissionless framework for protocols that allows anyone to launch a new perpetual futures market. Currently, HIP-3 accounts for approximately 35%-37% of total trading volume, representing a 600%-800% increase compared to the end of 2025. Open interest (OI) in these markets reached $1.7 billion in mid-May, an increase of over 150% since February. Commodities account for approximately $730 million of this, with crude oil alone accounting for about 20%.

The pace of change is rapid. Crypto trading pairs—the platform's original business—have dropped from approximately 90% to about 65%. Currently, five of the top ten traded assets are traditional market instruments, such as commodities. A platform that once focused solely on crypto derivatives is increasingly resembling a macro exchange.

Hyperliquid's bullish logic is built on this asset class diversification. With the launch of HIP-4 in early May, focusing on prediction markets and options, Hyperliquid is accelerating its transformation into an "exchange for everything."

Follow the money

Hyperliquid's data places it among the most profitable protocols in the digital asset space, even rivaling top traditional derivatives exchanges:

- Total historical trading volume: $4.22 trillion. Of this, $2.9 trillion occurred in 2025, comparable to CME Group's $3 trillion cryptocurrency derivatives contract trading volume.

- Total cumulative contract revenue: $1.15 billion. Revenue for the year 2025 is projected to be $873 million, compared to CME Group's $6.5 billion for the same period.

Furthermore, the HYPE token benefits from a continuous buying force and value return mechanism – the Assistance Fund. This fund channeles 97%-99% of the platform's transaction fees into automated token buybacks, with a total buyback amount exceeding $1.5 billion to date. This "stock buyback program" scales linearly with trading volume, requires no board approval, and each transaction directly impacts the token supply dynamics.

Based on the current operating pace, the implied repurchase yield is approximately 13% of the circulating market capitalization. For comparison, CME Group approved a $3 billion stock repurchase program at the end of 2024, but only used $532 million. This translates to an annualized yield of approximately $1.06 billion, corresponding to a market capitalization of approximately $105 billion, representing a yield of about 1%. Hyperliquid's return on capital is approximately 13 times that of CME, but the risk is also significantly higher.

HYPE serves as both a payment medium for transaction fees and collateral required for deploying new HIP-3 markets. Currently, each new perpetual contract market launch requires locking up 500,000 HYPE, worth approximately $19.5 million. As the platform expands to more asset classes, HYPE is being withdrawn from circulation from multiple directions simultaneously. Based on current trading volumes, the protocol is in a net deflationary state: approximately 1.95 million HYPE are being repurchased monthly, exceeding the approximately 1.75 million HYPE released through unlocking and staking.

Let's do the math.

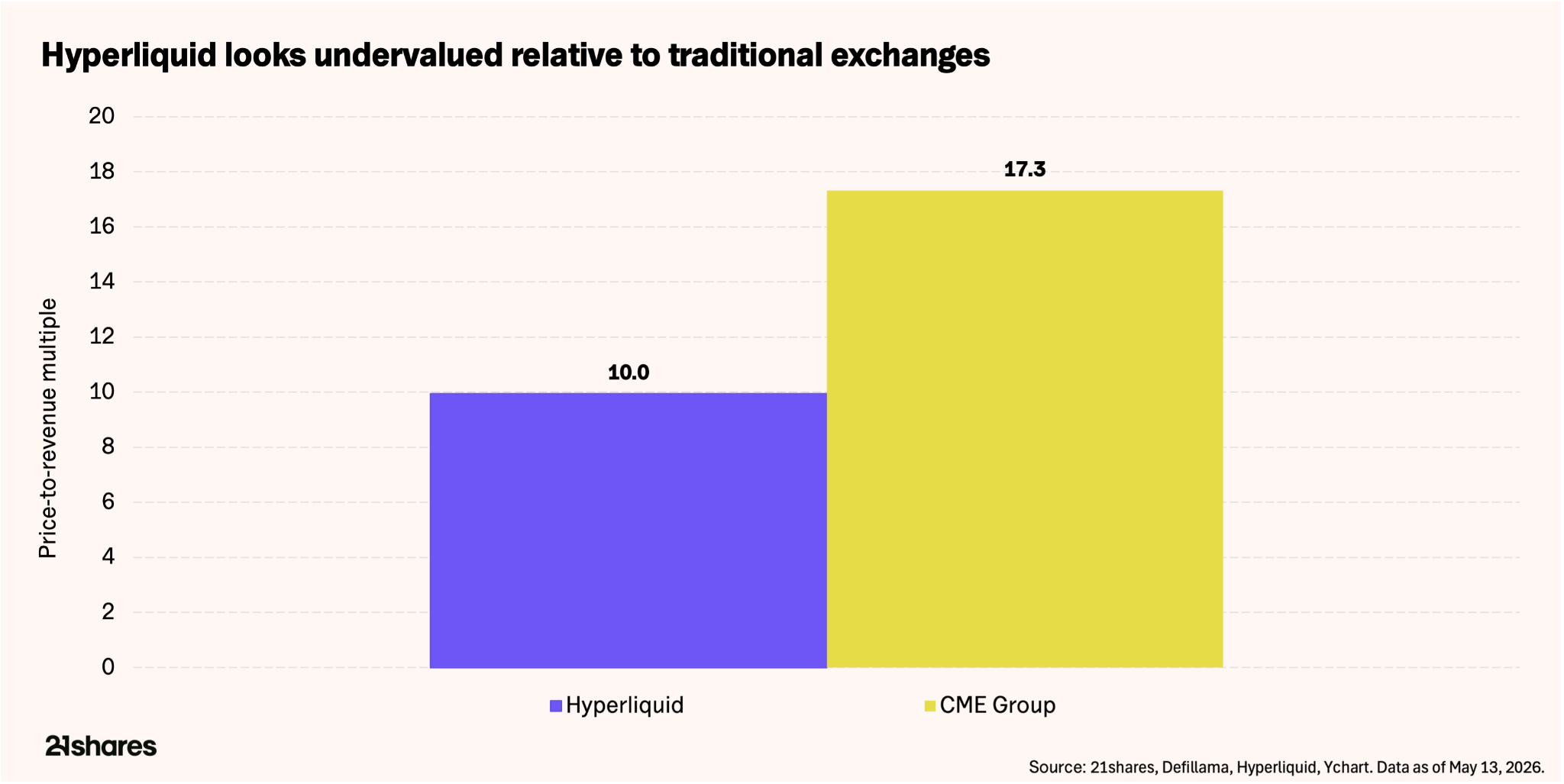

HYPE currently has a market capitalization of approximately $9.4 billion. Compared to its revenue of $944 million over the past 12 months, Hyperliquid's price-to-sales ratio (P/R) is approximately 10. In comparison, CME Group, the world's largest derivatives exchange, has a P/R of 17.32, a market capitalization of approximately $110 billion, and projected revenue of $6.5 billion in 2025.

Chart caption: Comparison of HYPE's price-to-sales ratio and revenue per employee with CME Group.

The market is already pricing HYPE using the valuation framework of traditional exchanges. The real question is whether Hyperliquid's revenue quality justifies this comparison. To illustrate the efficiency advantage of blockchain infrastructure over traditional systems: Hyperliquid's revenue in 2025 was $873 million, with a team of only 11 people—an average revenue of $79.36 million per person. CME Group's $6.5 billion in revenue was backed by 3,875 employees, an average of $1.7 million per person. The difference is obvious.

Based on a fully diluted benchmark—including all 1 billion HYPE tokens, most of which are still unlocked—the valuation jumps to approximately $37 billion, or 38-39 times revenue. This figure only holds true if revenue grows significantly before all tokens are in circulation. However, considering Hyperliquid's annualized user growth exceeding 100%, coupled with its expansion into new asset classes such as commodities and prediction markets, this growth premium may be reasonable.

Instead of giving a specific target price for a token, consider the following scenarios:

Bull Market Scenario: If geopolitical tensions persist and commodity trading remains high, traditional asset traders continue to flock to Hyperliquid after the market closes, HIP-3 open interest could grow to $3-5 billion, potentially generating $1.2-1.5 billion in annualized revenue. Based on a CME price-to-sales ratio of 16-17, this implies a market capitalization of approximately $15-17 billion, corresponding to a HYPE of around $62-70. Revenue could accelerate further if options and prediction markets gain traction in the coming months.

Baseline Scenario: Under similar assumptions, HIP-3 open interest grows to $3.2-5.3 billion, with annualized revenue reaching $1-1.1 billion. Based on a price-to-sales ratio of 17, the implied market capitalization is approximately $17-18 billion, corresponding to a HYPE ratio of approximately $75.

Caption: Comparison of three valuation scenarios (bull market/benchmark/bear market)

Bear Market Scenario: If non-digital asset trading cools down, buybacks may not offset token unlocks, causing annualized revenue to slide into the $350-450 million range. Using a more conservative 10x multiplier—reflecting slower growth and higher dilution—the market capitalization would be approximately $3.5-4.5 billion, corresponding to a HYPE of around $15-19, representing a 51%-62% pullback from current levels. However, this still doesn't account for revenue diversification from the upcoming prediction market and options trading.

The market is validating our bullish argument: Bitcoin is down 9% year-to-date, while HYPE is up over 50%. This decoupling stems from HYPE's shift towards diversified revenue streams. HYPE is not risk-free; it has simply replaced the risks of the crypto beta with geopolitical volatility. Whether this trend can continue depends on the geopolitical situation and the team's execution capabilities.

Risks that must be faced

HYPE has several core risks that investors need to weigh in conjunction with protocol growth:

Centralization and Attack Vectors: The 2025 JELLYJELLY and POPCAT token attack nearly emptied $230 million in liquidity, forcing validators to manually delist the assets. While effective, this exposed the possibility of platforms acting in a centralized manner when their funds are threatened.

Regulation: Hyperliquid still maintains geo-blocking for US users, and on-chain commodities exist in a regulatory gray area. To address this issue, HYPE may need to obtain a license, similar to Polymarket's acquisition of a CFTC-regulated entity to legally operate in the US market.

Geopolitical Shift: HIP-3's revenue benefits from global tensions. Cooling macro volatility could quickly erase the current "geopolitical volatility (VIX)" premium that drives the platform, thereby impacting token value.

Issuance vs. Buybacks: Although the protocol is currently in net deflation, its ability to absorb the continuous unlocking of tokens depends entirely on maintaining high trading volume.

in conclusion

The crude oil market is trading on the blockchain not because of decentralized ideals, but because all other markets have shut down. This distinction—practicality rather than ideology—is the fundamental difference between Hyperliquid's current situation and previous DeFi narratives.

With a valuation of 13-15 times annualized revenue, the market is pricing HYPE as a legitimate exchange business, not a speculative altcoin. The safety margin depends on the sustainability of non-crypto trading volume, whether buybacks can continue to outpace dilution, and the effectiveness of new feature implementation.

The data itself is at least worth a serious look at HYPE. Whether it's worth including in your portfolio depends on your judgment of the world beyond the charts.