Original author: Mario Chow

Original source: IOSG Ventures

TL;DR

- Why is pre-IPO perpetuity important? It opens two doors that were previously closed to almost everyone: one is placing directional bets on private companies like SpaceX and OpenAI *before* they go public, and the other is getting a real-time price on nights, weekends, and pre-market hours when the stock market is closed but news is still driving prices. Now, anyone with a wallet can place this bet continuously, without permission, and right in the middle of the biggest wave of IPOs in history.

- Without a publicly available spot price, how does the market price an item? This is the core problem the entire category needs to solve. Without external prices to copy (which can sometimes take months to replicate), exchanges can only use their own order book to create a price, and only allow it to move when there's real money willing to trade at a price deviating from it: slow and too expensive to fake. Trade.xyz uses an internal oracle plus a price range, while Ventures relies partly on primary market data. Surprisingly, this approach actually works: Yongxu predicted Cerebras' opening price within 1.3%, and even set a price for crude oil on a weekend when all traditional markets were blacked out.

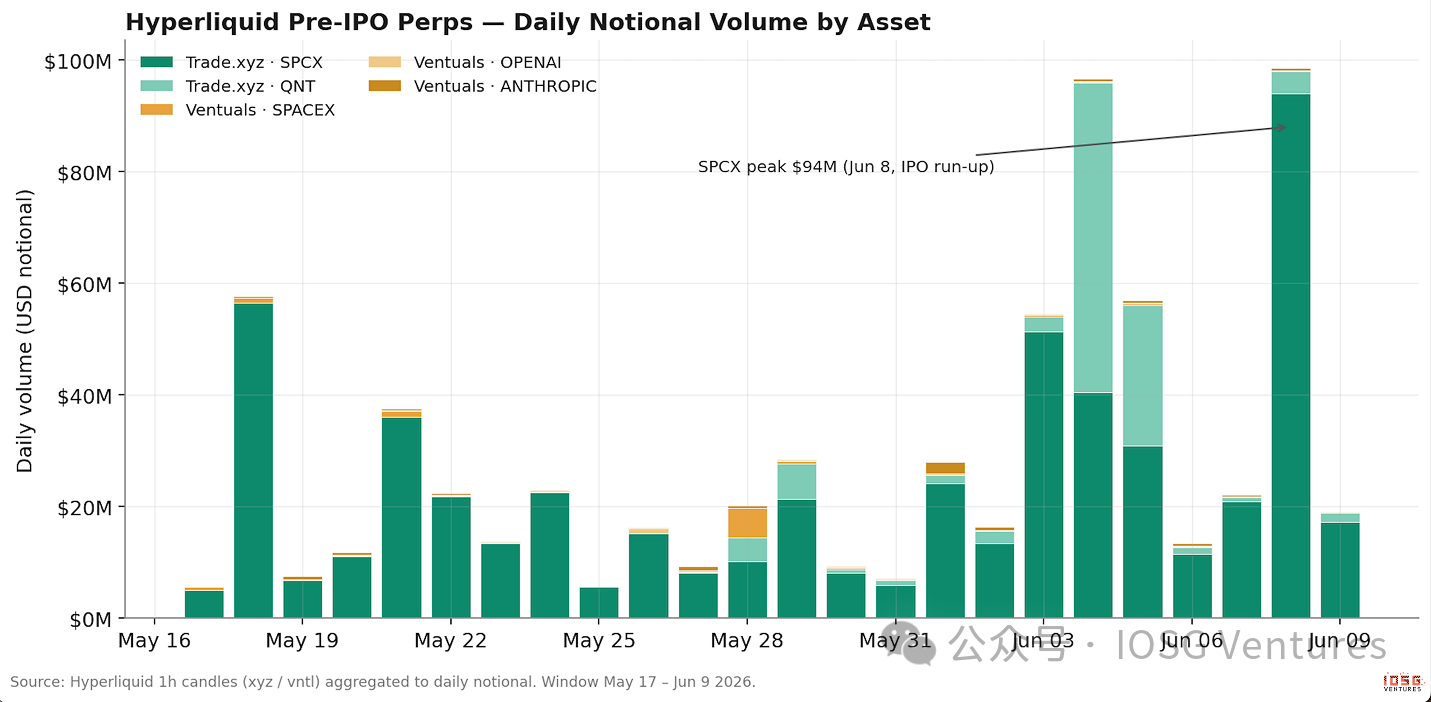

- What worked in the SpaceX case? Trade.xyz captured the on-chain market (approximately 96.5% of the trading volume), not because its oracles were smarter, but because the near-zero funding fees allowed the transaction to be held at almost zero cost. It launched *on* the IPO catalyst and, on a per-share basis, integrated cross-exchange arbitrage. On its listing day, June 12th, the switch from synthetic perpetual to tracking spot was clean: no oracle gaps, no liquidation waterfalls. On the listing day, perp closely followed the Nasdaq real-time price, with a difference of less than 1% (approximately $152 to $150 matching price); its pre-market mark price also happened to be right on Nasdaq's own opening indication price (approximately $175), and the final settlement price was even lower at $150.

- What risks remain unresolved? This category excels at price discovery but remains rudimentary in event handling. Corporate actions, particularly a stock split following a conversion, lack any on-chain infrastructure: trade.xyz hasn't published any rebase mechanism, and Ventures outsourced it to a single data provider that has already experienced a crash (an outdated split data point caused its market to plummet by 45%). The bottleneck isn't price discovery, but rather that tedious "corporate action" processing layer: traditional markets spent a century standardizing it, yet no one on-chain has rebuilt it. Whoever can reliably deliver it will fill the final gap between these markets and the ones they're replacing.

Background: Crypto had just kicked open two locked doors.

Pre-IPO perpetual contracts were stuck at the intersection of two things that, until recently, were almost entirely closed to everyone. Now, the crypto track has pried open both doors.

The first door: Pre-IPO access, finally open to retail investors.

Previously, pre-IPO shares of SpaceX or OpenAI were only accessible to accredited investors, venture capitalists, and a few secondary market participants. Valuations were opaque, and prices were only reclassified with each funding round. Pre-IPO perpetual contracts have dismantled this barrier. Anyone with a wallet can bet on the valuation of a private company, placing bets at any time, without permission, and without touching any shares, quotas, or voting rights. The timing is perfect; the largest wave of IPOs in history has just begun. SpaceX listed on Nasdaq on June 12th with a valuation of approximately $1.77T, and OpenAI and Anthropic are expected to follow suit. For the first time, retail investors can position themselves before the market opens, instead of chasing high prices after the IPO.

The second door: the after-hours session, is now under the control of crypto.

Traditional exchanges still adhere to "banker's hours." Stocks and futures are completely shut down at night, on weekends, and on holidays, so once news breaks after the market closes, there's nowhere to hedge the real risk exposure. Crypto exchanges, on the other hand, never close, giving them the entire after-hours window, and most price discovery happens on Hyperliquid.

The key premise of this report is that the after-hours quote isn't just guesswork; it often falls precisely where the actual market reopens. For example, on a Saturday when Middle East conflict pushed up oil prices, only Hyperliquid was trading in the entire market. When CME crude oil futures reopened on Sunday evening, the opening price was exactly the one Hyperliquid perpetual had already found. TD Securities estimates that before traditional exchanges even opened, this platform had already absorbed about 80% of the recent oil price volatility. The same applies to stocks; the Cerebras perpetual contract on trade.xyz ultimately opened at only about 1.3% lower than the Nasdaq price. In the after-hours session, the perpetual contract itself is the market.

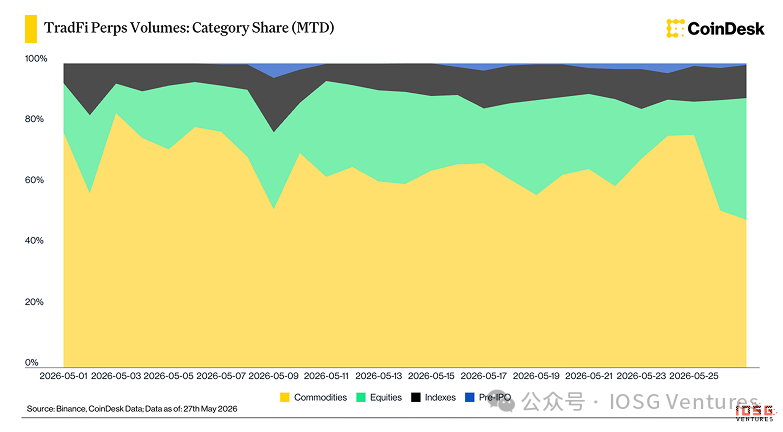

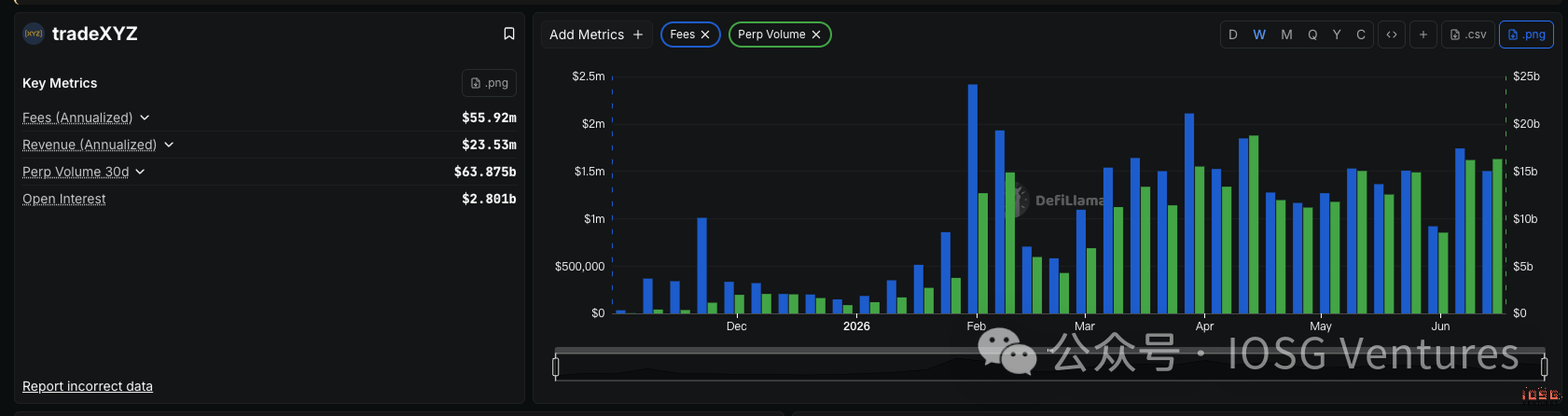

How early is it: It only accounts for about 1% of TradeFi's perpetual contract trading volume.

CoinDesk's data shows just how early this market is. In Binance and similar platforms' TradeFi perpetual contracts, commodities and stocks dominate. Pre-IPO is just a thin strip at the very top of the stack, accounting for just over 1% of the total trading volume of TradeFi perpetual contracts since its launch around May 21.

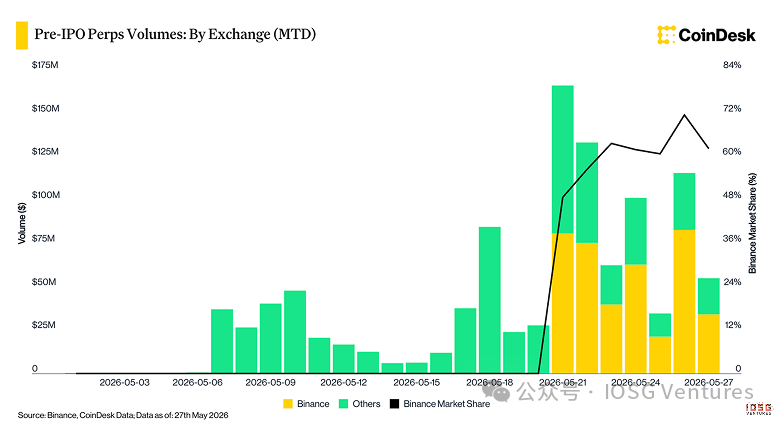

On Binance, pre-IPO trading volume is also highly concentrated on a few specific stocks: SpaceX accounts for approximately 79%, OpenAI 11%, and Anthropic 9%. This category only launched around May 20th, and Binance quickly captured over 60% of its share. Pre-IPO trading on CEXs is still in its infancy, with SpaceX as the main player. The truly interesting activity is on-chain.

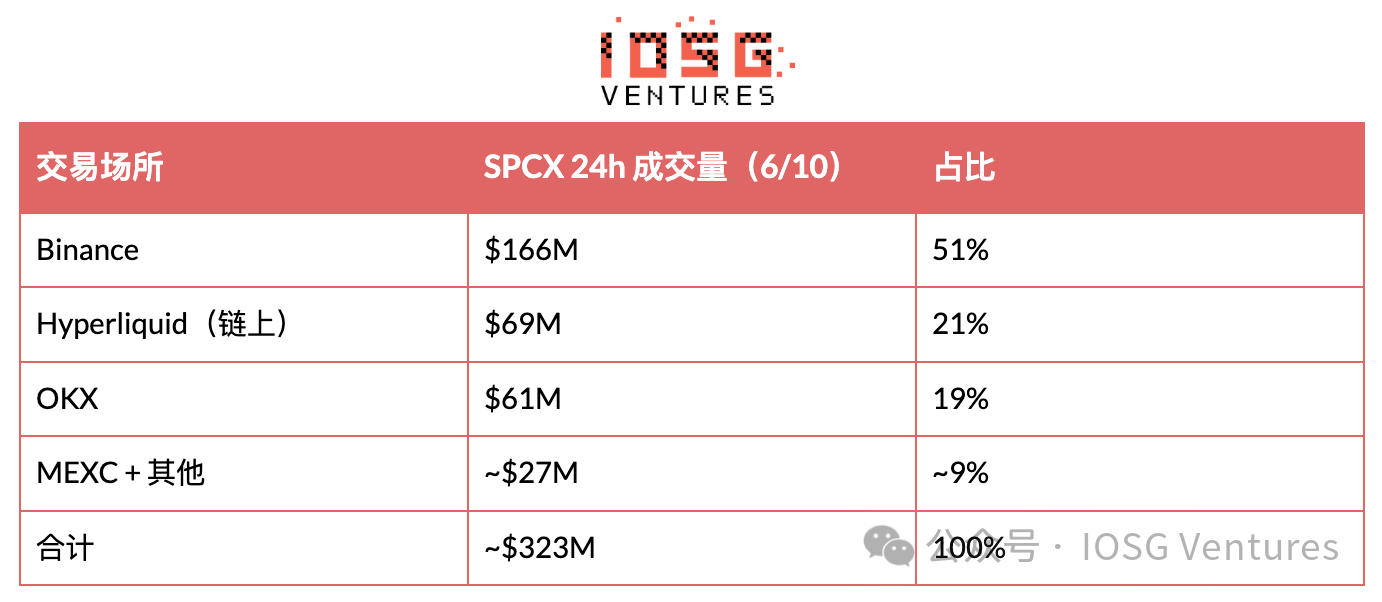

SPCX's position across various exchanges: Binance leads, Hyperliquid firmly holds its on-chain dominance.

Market snapshot on June 10

Focusing on SpaceX itself, it is currently the entire pre-IPO market. In this snapshot from June 10th, the total 24-hour trading volume of SPCX was approximately $323 million. Binance led with $166 million (51%), followed by Hyperliquid with $69 million (21%), OKX with $61 million (19%), and then MEXC and a bunch of smaller venues.

On-chain landscape: A market with only one builder

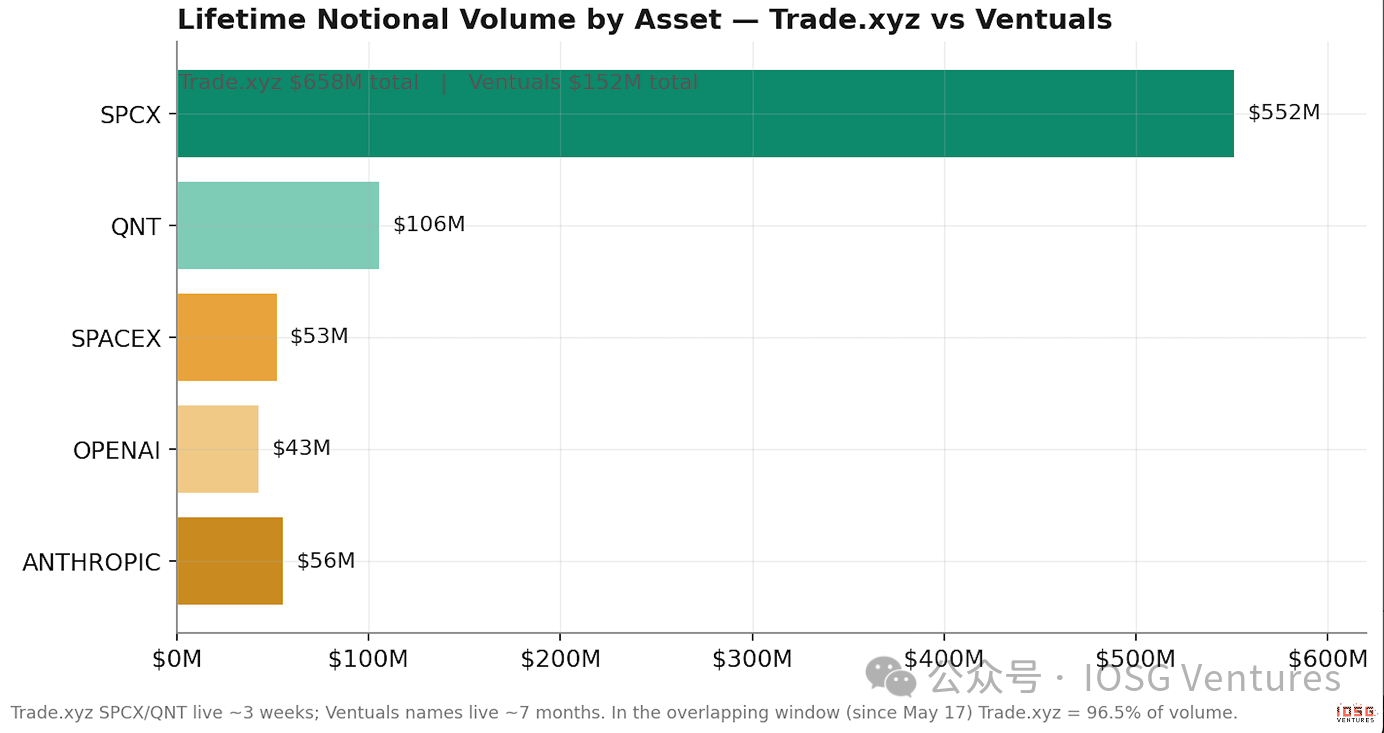

Comparing Trade.xyz and Ventures using data: 96.5% vs. 3.5%.

Trade.xyz's total trading volume was approximately $658 million, with SPCX accounting for $552 million and the second asset, QNT, for $106 million, all crammed into about three weeks. Ventuals' total trading volume was approximately $152 million, more evenly distributed across SPACEX ($53 million), OPENAI ($43 million), and ANTHROPIC ($56 million), taking about seven months.

Placing both on the same timeline makes the difference immediately apparent. Within the overlapping window after SPCX's launch, trade.xyz accounted for approximately 96.5% of on-chain pre-IPO trading volume, which corroborates the third-party tracking agency's estimate of "approximately 95% of the Hyperliquid pre-IPO basket." Ventuals listed more tokens, including the currently only online Anthropic and OpenAI contracts, but only received a small share of the traffic. Listing tokens isn't a moat; liquidity is.

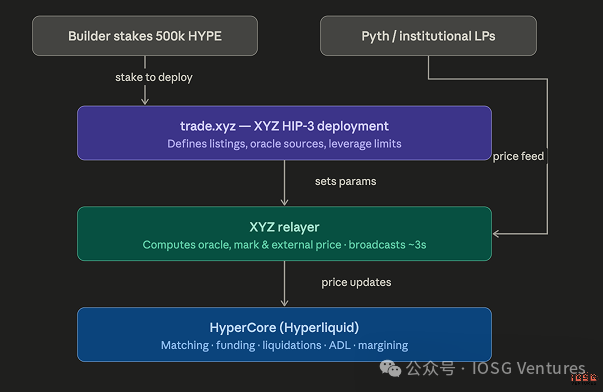

HIP-3: The platform layer beneath all of this

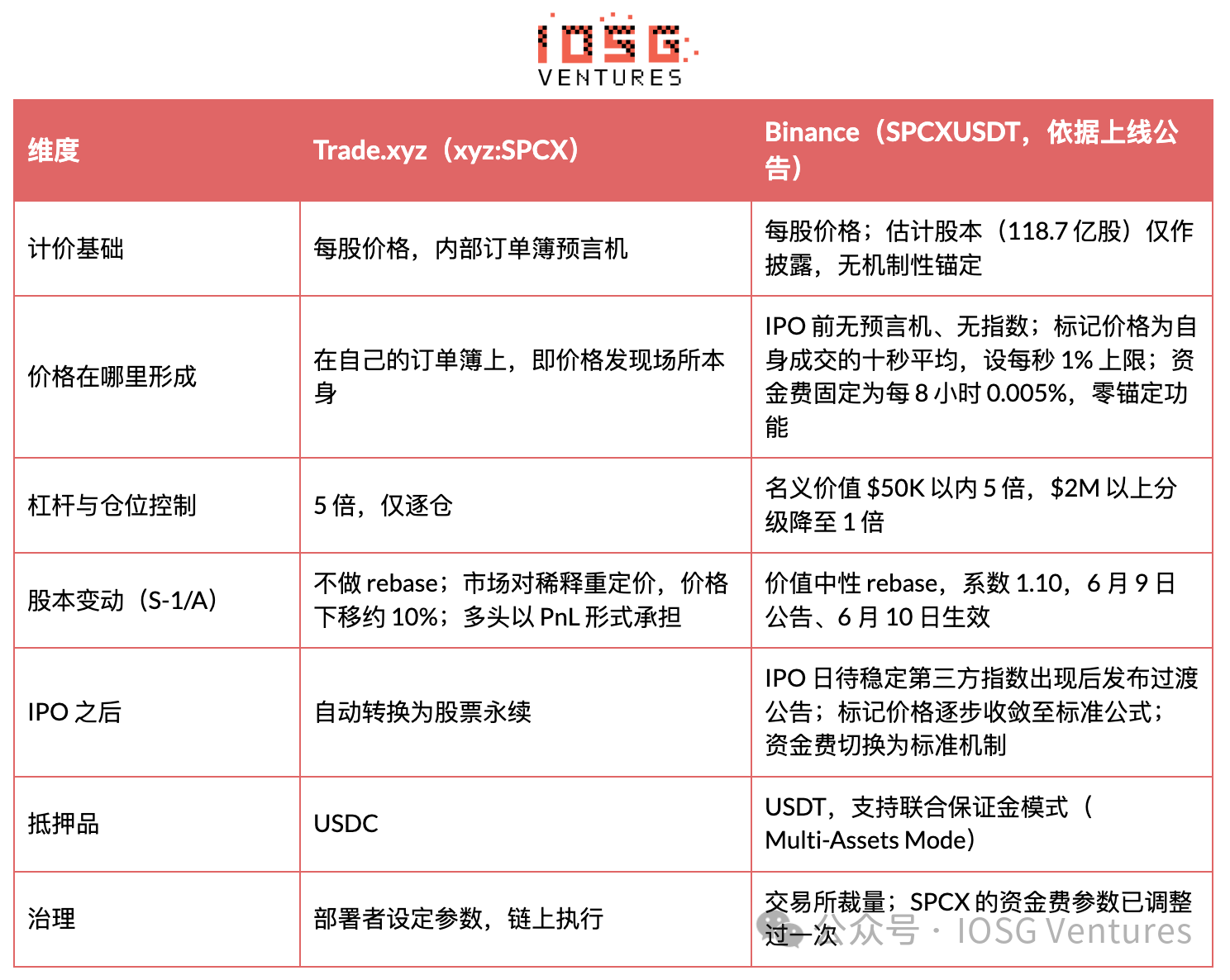

HIP-3 is an upgrade to Hyperliquid that transforms a single perpetual contract marketplace into a platform for builders to deploy perpetual DEXs. Any team staking 500,000 HYPE can deploy its own perpetual market on HyperCore, Hyperliquid's matching layer. Builders control listings, oracles, leverage limits, and contract parameters; HyperCore controls execution, funding fees, liquidation, and margin. Trade.xyz focuses on HIP-3 deployments for traditional assets: creating 24/7 perpetual contracts for stocks, indices, and commodities, with margin and settlement in USDC, and only supporting isolated margin.

How does Trade.xyz price the market when there is no external truth value?

Let's start with the problem, because only by understanding the problem can this design make sense. Regular perpetual bonds copy a real-time spot price from the exchange; pre-IPO perpetual bonds have no spot price to copy at all, and there might not be one for months. Therefore, the exchange can only use its only resource—its own order book—to create a credible price, and it has to be expensive enough to be difficult to manipulate. This entire section answers the same question: how do you price an asset when it doesn't yet have a price?

Two sets of oracle mechanisms for perpetual stock trading after hours

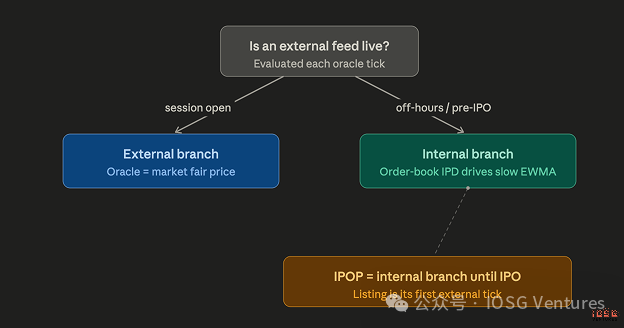

To understand pre-IPO permalinks, one must first understand after-hours stock permalinks. Crypto permalinks have real-time external prices 24/7, while stocks do not. AAPL only has a true market price during US stock trading hours, so oracles supplying funding fees and markup prices need two mechanisms: one for when external data is available, and another for when it's unavailable. When the external market opens, the relayer directly inputs the institutional fair price (data sources include Pyth) as the oracle. When the market is closed, the oracle can only continue processing using the permalink's own order book; this is the most ingenious part of the entire design.

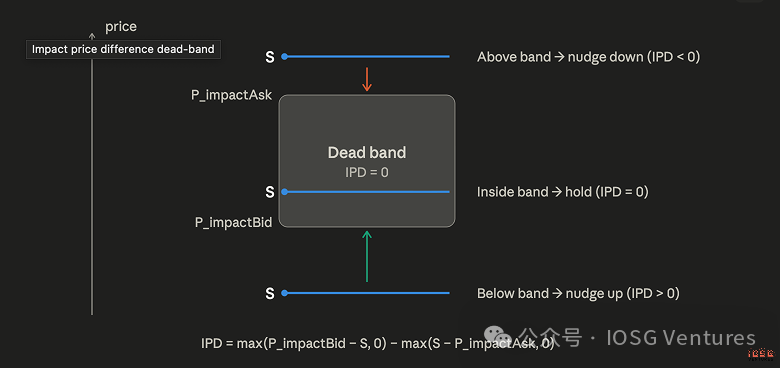

Internal Oracles: Three Core Ideas

Check where the order book for transactions is located.

The repeater calculates the average execution price of a fixed $1,000 order pushed to each side of the order book, thus determining the executable bid and ask prices. If the current oracle price falls within this range, nothing happens—the order book matches the oracle, and the oracle remains unchanged. The oracle is only pushed into the order book when the price falls outside the range, meaning the actual order book depth is willing to execute at the deviated price. Heavy buying pushes the price up, heavy selling pushes it down, and noise within the range is completely ignored. To push this oracle forward, real liquidity must be injected, not just a few trades.

Oracles never change.

It slowly converges to the order book with a 30-minute time constant, and a hard cap ensures that a single update can only converge to about 9.5% of the remaining distance, regardless of how much time has passed since the last update. Suspension and irregular updates cannot cause it to jump.

The median price is used as the price marker.

The mark price driving margin and liquidation is the median of three candidate values: the oracle itself, the short-term moving average of the oracle plus the perpetual contract basis, and an order book snapshot (best bid, best ask, and latest traded price). This median structure means that the fast variable itself can never drag the mark price too far away from the slow oracle. Hourly funding fees further push the market towards the oracle, with standard multipliers and caps ensuring that any single hourly payout is small.

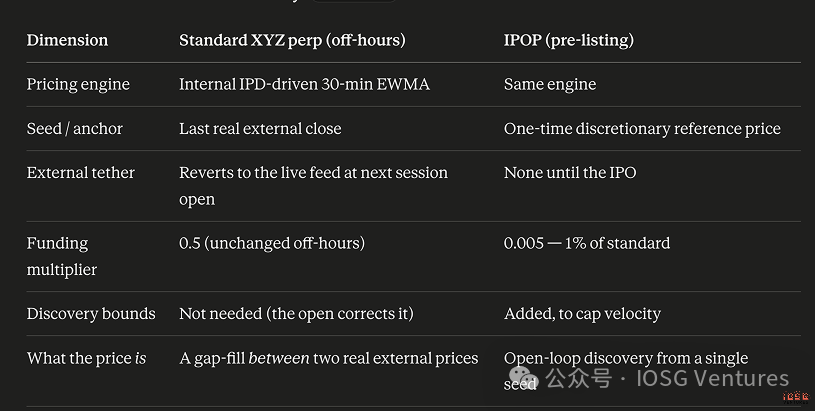

Pre-IPO Sustainability: Same Engine, Three Changes

IPOP (Pre-IPO Perpetual Contract) is essentially an after-hours stock perpetual contract that never has a "Friday closing price" to rely on. There is no external price before listing, so the market must continuously operate its internal pricing mechanism, sometimes for months. Trade.xyz made three changes to address this, each revealing the essence of the problem.

- Funding rates have been slashed to 1% of the standard rate. Perpetual contracts drift for a maximum of two days over the weekend, correcting themselves at Monday's opening, so normal funding costs are tolerable. IPOP could trade for over sixty days without any anchor, and the market often remains at a persistent premium or discount reflecting pure sentiment. Under the standard rate, anyone holding a position against the mainstream sentiment would be bled dry by funding costs long before the IPO. Slashing the multiplier to almost zero makes this contract truly tradable. Our view: More than any clever oracle design, it is this single parameter that makes trade.xyz's products tradable, a point confirmed by the funding data later in this report.

- Initial seed price. The weekend market initialized with the last real external price. IPOP has no history, so trade.xyz set its own initial reference price. It's not a prediction, just a mathematical starting point. Taking SPCX as an example (launching late UTC on May 17th), the reference price was set at $150 per share: taking the midpoint of SpaceX's publicly reported target valuation of $1.75T–$2T, divided by the assumed 11.87 billion fully diluted shares.

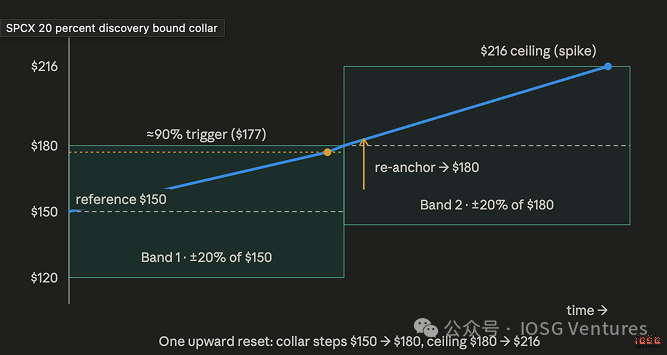

- Discovery bound. A price range (collar) around the reference price and the marker price that must not be exceeded, with a rule that positions whose liquidation price falls outside the current range will not be liquidated during the range's validity period.

For SPCX with 5x leverage, the range width is 20% above and below. Static ranges either freeze prices or are ineffective, so this range is stepped: when the slow oracle climbs to 90% of the upper limit, the reference price is re-anchored to that upper limit, and a new 20% range is opened around it.

SPCX has seven such tiers in each direction. Combining the tiers, the hard lifetime range for the contract, starting from a seed price of $150, is approximately $25 to $645 per share.

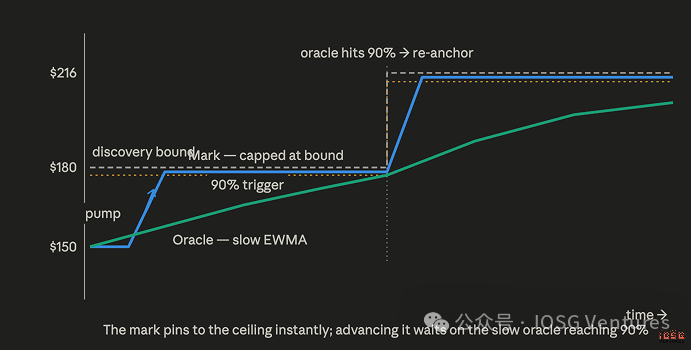

How much does it cost to manipulate this market: expensive, conspicuous, and slow.

This division of labor is crucial for anyone who wants to manipulate the market. The mark price reacts quickly but has a hard ceiling; a single pump can almost instantly slam it to the ceiling, and then it freezes there.

The oracle, representing a slow 30-minute average, is the gatekeeper: the ladder only moves up when the oracle reaches the 90% trigger line. To push the price up one level, an attacker has to withstand arbitrage trading and keep the entire order book elevated for nearly an hour, then repeat the process for the next level. Expensive, conspicuous, and slow—that's the design intent, and so far it has held up remarkably well.

Two builders: Trade.xyz and Ventures

Ventuals: Partial Trust in External Data

The pre-IPO perpetuity on Hyperliquid comes from two HIP-3 builders who answer the same question from opposite directions. Trade.xyz trusts its own order book; Ventuals partially trusts external data. Ventuals prices valuations rather than stock prices: a SPACEX price of 1,989 implies a market-implied valuation of $1.989T for the company. Its oracles are a weighted mix: one-third from external valuation estimates from Notice.co, and two-thirds from a two-hour moving average of Ventuals' own marked price.

The Notice aggregates secondary market data, order book quotes, financing announcements, mutual fund valuations, 409A valuations, and comparable listed company data, polling at least once per minute. That deliberately set one-third weighting is Ventures' answer to the "IPO bubble problem": anchoring to the realities of the primary market while allowing the market mathematical space for upward pricing. And don't overlook this: two-thirds of this oracle is Ventures' own market; this design is far more self-referential than its marketing rhetoric suggests.

Its anti-manipulation mechanism is built on the price path, not on a range ladder. Orders cannot deviate from the oracle by more than 20% and are enforced by the matching engine. The mark price is updated every three seconds, with a maximum change of 1% each time. Once a short-term shock causes the price to deviate from its one-minute average by more than 2%, the mark price update coefficient immediately resets to zero. Therefore, sudden volatility must persist for the mark price to follow. Funding fees are dynamic: approximately 15% annualized when the market is close to the oracle, increasing exponentially as the deviation widens, approaching 1% per hour when nearing the edge of the range.

The endgame design is also completely different. When a company goes public, the Ventures market settles and stops: funding fees are zeroed, the mark price is forcibly rewritten to reflect the valuation implied by the first day's closing price, and all positions are forcibly liquidated. It's more like a prediction market betting on the closing price on the first day of listing than a perpetual contract. Trade.xyz's IPOP, on the other hand, is directly converted into perpetual ordinary shares and continues to trade.

Side-by-side comparison

Why early adopters lost: Cost of holdings, oracle malfunctions, and missing catalysts.

Ventuals launched in November 2025, six months earlier than any of trade.xyz's listings, and still holds the only online OpenAI and Anthropic contracts. It currently accounts for only about 3.5% of on-chain pre-IPO trading volume. The explanation lies primarily in its mechanism design, two parts of which can be directly quantified.

Cost of holding

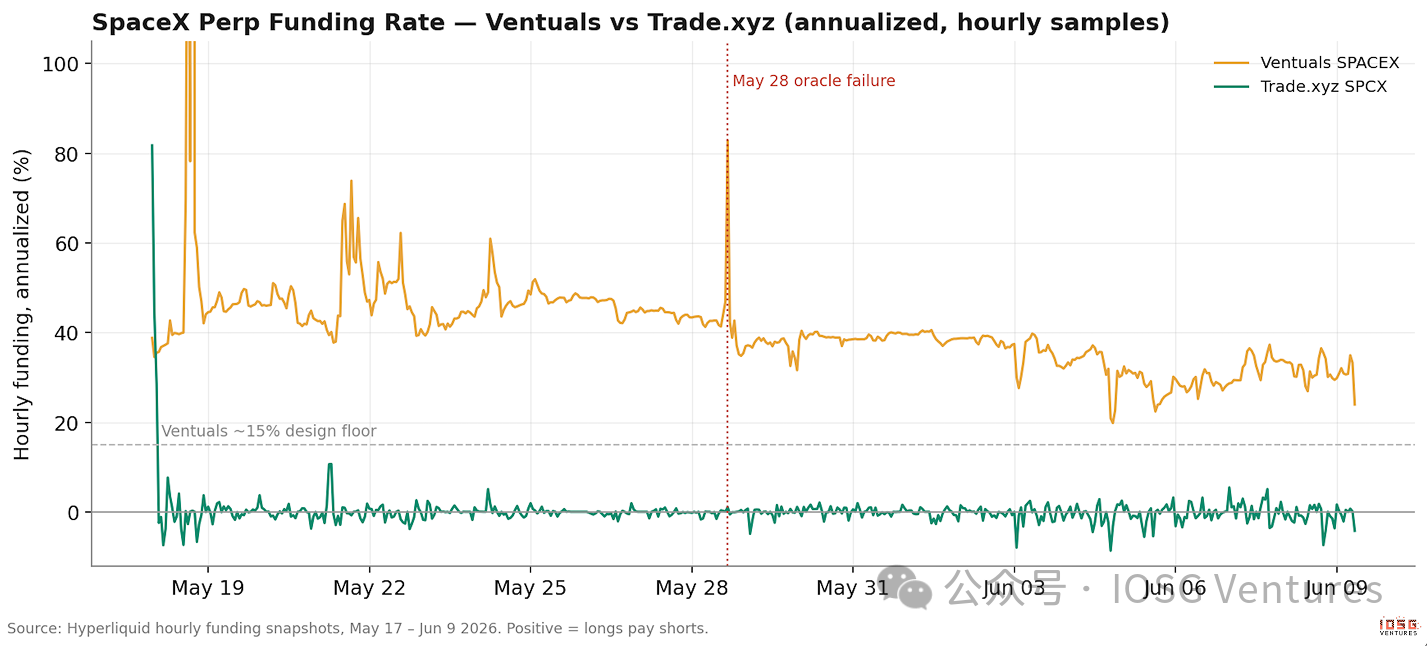

The two funding fee designs imply a vastly different cost for holding a pre-IPO view, and actual funding fee data shows the gap is even larger than the documentation suggests. Over the exact same 538 hours from May 17th to June 9th, SpaceX long positions on Ventures paid funding fees every hour, averaging approximately 45% annualized, with a cumulative cost of 2.79% of the notional value. The same long positions on trade.xyz paid only 0.008%. The average funding fee on Ventures was 33 times higher, and the cumulative cost was approximately 350 times higher.

With standard 5x leverage, Ventures' losses amount to approximately 14% of the margin being wiped out over 23 days, precisely in the very transaction upon which both venues depend: a long position in SpaceX before its IPO. Holders provided liquidity to attract everyone's orders, resulting in one venue charging them rent while the other didn't. We believe this is the single largest reason for the divergence in trading volume.

Looking at the full historical data, this becomes even more glaring. Long positions held since its November launch have cumulatively paid approximately 45% of their notional value in funding fees, as the market traded at a premium above the Notice anchor price for several months, with the dynamic multiplier charging for this throughout. This design allows price discovery above the anchor, much like a toll road allows you to drive.

Oracle malfunction

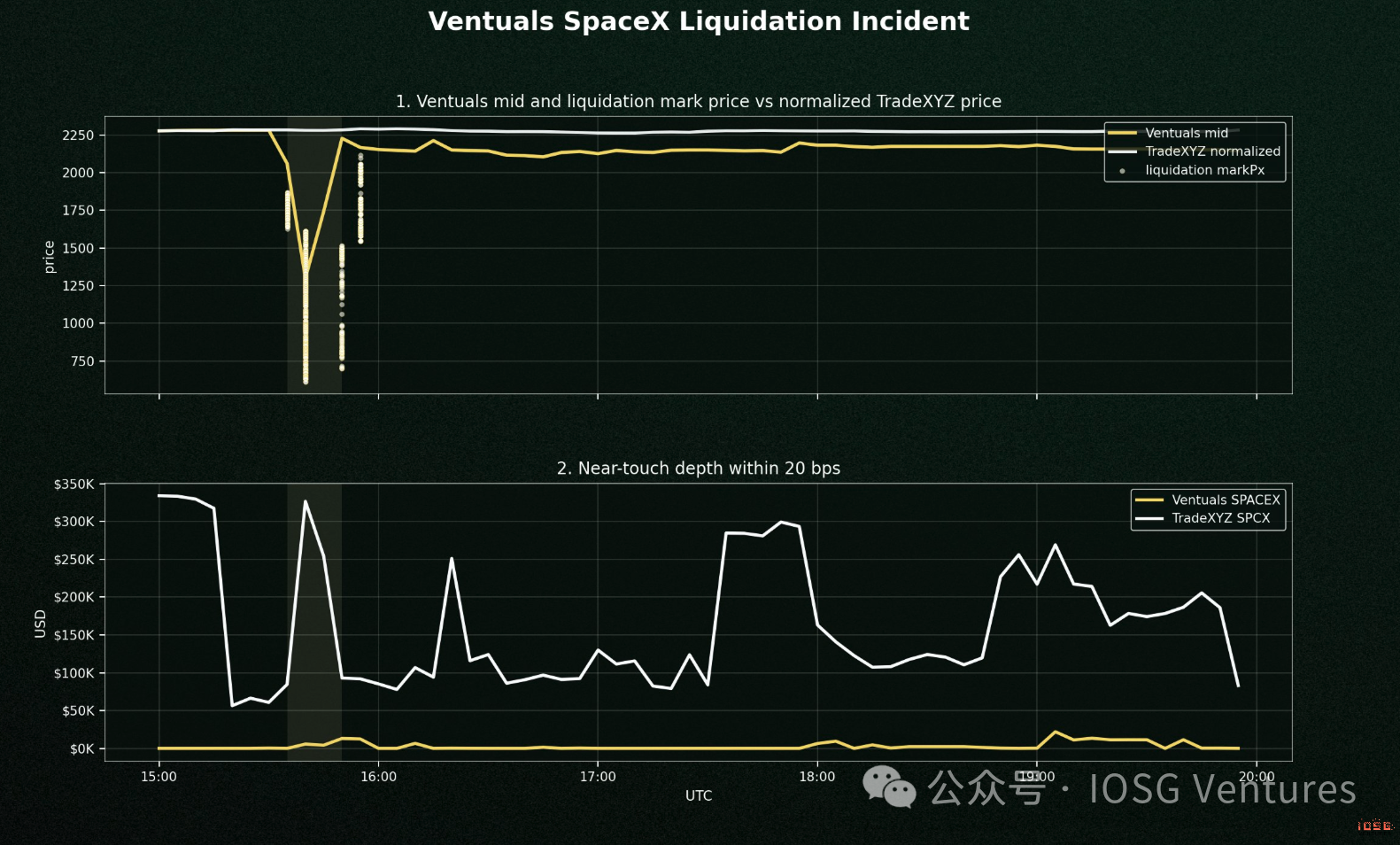

Ventuals relied on only one external data provider, and that provider ran into problems. SpaceX's 5-for-1 stock split, executed between May 18th and 22nd, was not correctly incorporated into Notice's data source. This bad data flowed directly into the oracle, which drove margin calculations, causing a deliberate flash crash of approximately 45% on SPACEX-USDH on May 28th, resulting in the liquidation of about $1.5 million before recovery.

The truly crucial detail is that all of Ventures' protection mechanisms are defined relative to the oracle. Therefore, if the oracle itself becomes the source of failure, every protection will re-anchor to that failure. The speed cap didn't prevent the crash; it merely scheduled it. With 1% compounding every three seconds, the entire 45% cycle was completed in about three minutes. Worse still, the 20% order price range effectively blocked any rescue: arbitrageurs, knowing the price was wrong, couldn't place orders beyond 20% above the faulty oracle, according to the rules. Trade.xyz wouldn't have crashed like this before its IPO for a simple reason: it simply didn't have any external data sources that could be contaminated. Its corresponding weakness is slow self-referential drift; ranges can constrain it, but they can't eliminate it, and this weakness hadn't yet reached its "accident" stage.

Three quieter forces concluded the battle.

All major centralized exchanges (CEXs) use per-share pricing, the same unit as trade.xyz. This allows its order book to directly arbitrage with each CEX screen, while Ventures' valuation unit excludes it from the arbitrage network. It turns out that demand for this type of product is event-driven rather than consistent. Launching six months early on SpaceX didn't bring much benefit to Ventures, while trade.xyz benefited from the catalyst. Furthermore, Ventures' "settlement-stop" policy effectively tells market makers in advance: your market is dead on listing day. Cerebras data shows that the trading volume arrived precisely on that day; approximately 85% of the contract's lifetime trading volume occurred on the IPO day.

What did Ventuals still do right?

All of this doesn't mean that Ventures' design is wrong. Its dilution-resistant valuation unit requires no rebase when the S-1/A is finalized; its funding fees, in terms of "anchoring," are arguably more honest than trade.xyz's near-zero rate, since the latter leaves the price unattached to any range. Cheap holdings and unanchored drift are two sides of the same design choice. But putting together the high holding costs, a publicly reported oracle failure, an isolated pricing unit, and a market structure where the endgame is inevitable, fully explains why a six-month initial offering only yielded a 3.5% market share.

CEX layer: Binance to Trade.xyz

No oracles, no indexes: Binance's design

Several major centralized exchanges (CEXs) entered the market relatively late. Binance launched SPCXUSDT on May 21st, three days later than trade.xyz, and its launch announcement detailed the design. Prior to the IPO, there were no oracles or indices. The mark price was simply the average of Binance's own transaction prices over the last ten seconds, calculated every second, reverting to a longer window during quiet periods, with a 1% fluctuation cap per second. Because there was no premium index, funding fees had no corrective function: a fixed 0.005% every 8 hours, approximately 5.5% annualized—a pure holding fee with no anchor. Long positions held from launch until June 9th paid approximately 0.29% of the notional value; this fixed cost was completely insensitive to everything that happened during that period (including dilution and repricing).

Therefore, of the three designs, Binance's is actually the most self-referential. Trade.xyz at least used its order book to build an oracle; Binance's price is simply the transaction price in its own order book, then smoothed over ten seconds. What makes it stable? A lenient speed cap, an adjustable but undisclosed maximum price limit, plus leverage that decreases based on position size: 5x only for notional values under $50,000, reduced to 1x for over $2,000, and requiring a 50% maintenance margin. Binance's whale control plays the same role that trade.xyz played in discovering the boundaries on-chain.

Corporate Action: A Watershed Moment in Two Philosophies

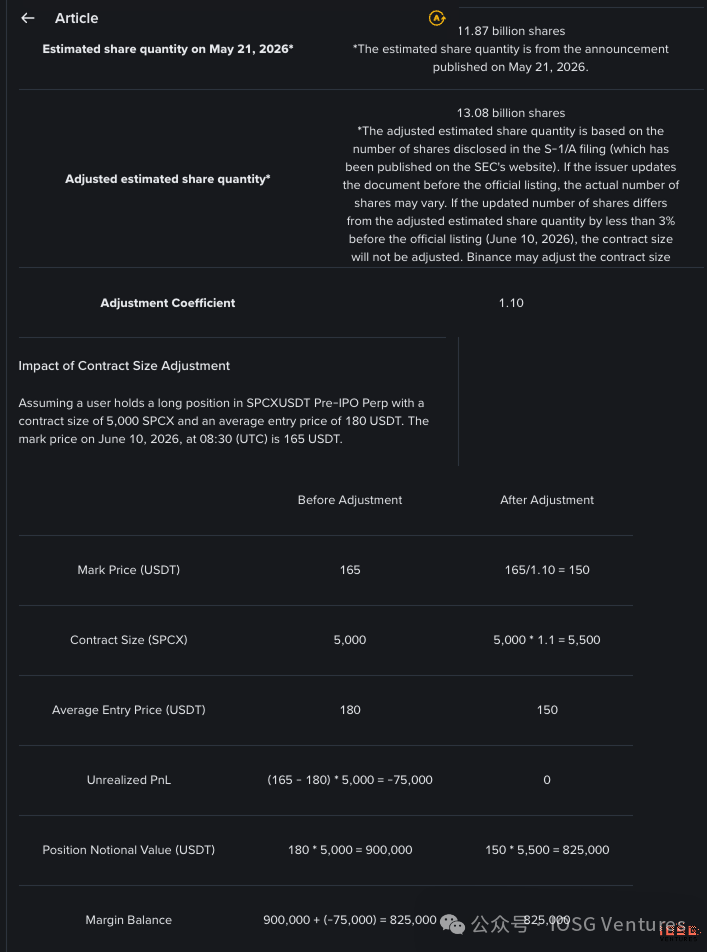

Trade.xyz treated the S-1/A share capital change as information, allowing the order book to repric itself, thus the longs absorbed the 10% dilution as PnL. Binance treated it as an administrative event: a value-neutral rebase with a coefficient of 1.10, contract size multiplied by 1.1, and opening price divided by 1.1, announced on June 9th and effective on June 10th, with each account's equity remaining unchanged. Neither approach is free.

Binance protected its holders by shielding them from the dilution of PnL that was never contracted, but this created a ten-day window during which its price was mechanicically 1.1 times that of trade.xyz, the premium seen in the venue snapshot. This cross-venue price split is essentially a rebase time difference map.

Adjusted results:

The Gap Where No One Priced It: trade.xyz Has No Answer for Stock Splits

The rebase debate above masks a more complex issue, one that falls on the side of trade.xyz. Pre-IPO capitalization restatements can be moved without a rebase: the S-1/A caused SPCX to fall by about 10% in repricing within days; the market did its job, and the losses incurred by the longs were at least related to value information. Post-conversion stock splits are a completely different species: a split changes the unit, not the value. A 5-for-1 split would divide the external stock price by five overnight, while the post-conversion xyz perpetual is designed as a price tracker with a real-time external oracle. Going through the published mechanisms, nothing can stop it: as long as the external data source is online, the internal IPD and EWMA mechanisms are bypassed because the oracle only transmits the external price; the discovery boundary only takes effect during the internal pricing period, not at the opening; the mark price is anchored to the oracle's median, so it will gap up. The result is mechanical: 80% of oracle gaps liquidate all long positions (regardless of the opening price), giving short sellers a windfall, and leaving the remaining exposure to ADL. Funding fees can't save it; they correct a basis on an hourly scale, whereas this is a unit change within a tick.

This is not a hypothetical risk profile. SpaceX itself executed a 5-for-1 stock split in the week of May 18th, the very event that poisoned the Ventures data provider; and high-priced publicly traded companies are precisely the most fond of stock splits: Nvidia, Amazon, Tesla, and Apple have all done so in recent years. The answer is in every other area of this report: the options market adjusts contract terms to ensure holders maintain an equivalent economic position after the split; Binance and OKX have announced rebase mechanisms and have already implemented them in a value-neutral manner on this particular asset; Ventures doesn't encounter this problem at all, as valuation-based contracts are inherently resistant to splits, and its market is settled before the company is listed. Trade.xyz's documentation details oracles down to the decimal point but makes no mention of individual company actions. Only its index products absorb company actions, and that's only because index futures do this upstream.

On a deeper level, this incident impacts the "conversion and continuation" selling point. Continuity is trade.xyz's signature advantage over Ventures: your market can survive past the IPO. However, a perpetual market that continues to exist after listing must take over the entire corporate calendar of the listed company: splits, special dividends, further splits, code changes, and trade.xyz is the only one in this comparison that hasn't published a mechanism for any of these. If something goes wrong, the venue will likely have to close and manually adjust positions. Deployers already have the authority to modify parameters, and the HIP-3 market can also be suspended. But this is precisely the kind of control room intervention that trade.xyz's "code over discretion" philosophy opposes most, and it happened at the worst possible time: user margin is tied up online, and there are no pre-published precedents to refer to. Our view: this is the most serious unresolved hidden danger in the entire design. Fixing it is actually very cheap; just publish a set of rebase precedents before the split after the first conversion. The fact that neither the documentation nor the market has yet priced it precisely illustrates how young this category is. To add to that, the honest conclusion is: trade.xyz is a safe bet if it survives the IPO, but not if it survives a split; and almost no one actually trading it knows this.

Side-by-side comparison

IPO Day: The First Real-World Test of the Mechanism (June 12)

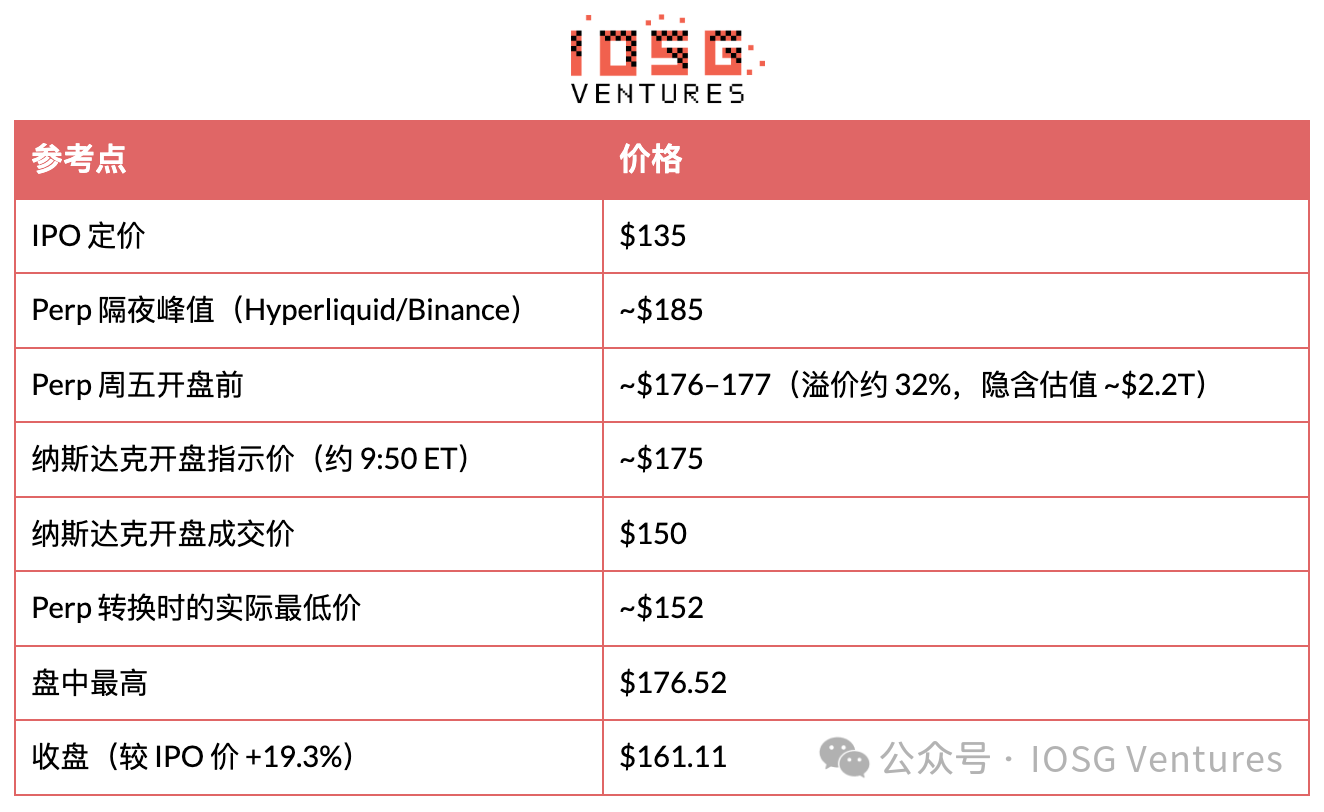

SpaceX debuted on Nasdaq on June 12th under the ticker symbol SPCX, priced at $135, offering 555.6 million shares and raising $75 billion—the largest IPO in history—making Elon Musk the world's first trillionaire. The stock opened at $150, reaching a high of $176.52 during the day, and closed at $161.11, a 19.3% increase for the day. At the close, it was the sixth-largest publicly traded company in the United States. For the venues covered in this report, this listing moment was precisely the moment all mechanisms had been preparing for. Here's what actually happened.

Price tiers: Eight price ranges, 37% across.

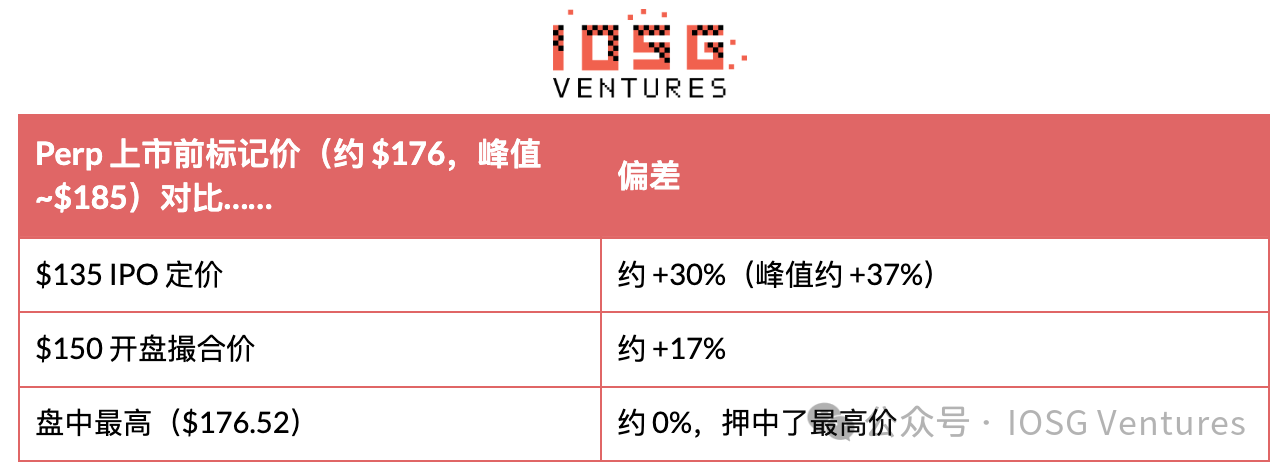

The most important point about this table: the eight reference points range by 37%, from the IPO price of $135 all the way to Perp's peak of $185; only the post-IPO cluster ($150–176.52) truly squeezes into the top 20%. Which one you call the "answer" determines whether Perp passes the test this time.

The Oracle switchover was successful, and the window we marked does indeed exist.

The conversion itself was clean. trade.xyz's SPCX perp switched from internal order book pricing to Nasdaq's real-time data source at market open, converting pre-IPO contracts into standard stock perpetual contracts without closing or reopening, ensuring seamless position continuation. Coinbase International's USDC-settled SPCX perp also completed the switch in the same way. There was no repeat of the Ventures incident on May 28th; there were no oracle jumps during the switch, and no reported large-scale liquidation crashes. This most leverage-sensitive moment in the product's lifecycle was safely navigated without structural failure, which is the most important result for the entire category that day: the convert-and-continue strategy worked.

However, the gap we marked before the IPO—the window of "listed but not yet priced"—did exist, and it was quite long. The opening bell at 9:30 ET was merely a ceremony; no trading took place for SpaceX. Nasdaq's opening auction, with its massive 555.6 million shares—the largest matching pool in IPO history—was manually adjusted by the underwriters, effectively dragging on for several hours. Nasdaq President Tal Cohen stated that it would take "a few more hours" for an orderly opening, and by 10:38 ET, not a single trade had been executed. The first trade price wasn't displayed until around 11:30 ET, roughly two hours later (the same pattern as the 2012 Meta listing). Throughout the window, Nasdaq continuously broadcast an indicative matching price every second, but no trades were executed. For about two hours, SpaceX was a publicly traded company with no available price, and trade.xyz's own documentation (according to its clarification on June 10) never specified how Perp priced its orders during this transition window. This time, nothing went wrong, for a specific reason: the opening auction wasn't a black box. Nasdaq broadcast a continuously updated order price every second throughout the auction, and that order price ($175) coincidentally matched Perp's own markup price ($176) for the entire period. However, there was a subtle point: Perp's oracle wasn't reading this order price at all. Its external data source (Pyth) only recognized already traded prices, and since there were no trades yet, it remained on its internal order book for the entire time, only switching when the first trade ($150) was executed. The coincidence between the two was purely coincidental, not linked, which is precisely why this undefined window didn't cause any problems. However, if there is a disorderly opening, such as suspension of trading, significant deviation of the indicative price, or delayed bidding, the damage will fall on the same unrecorded window, and this hole in the document has not been patched to this day.

Can the bids be tracked? How much difference is there in the perp?

Yes. Bidding can be tracked in real time because Nasdaq continuously publishes the opening price indication during the matching process. The more difficult question, and the key to this report, is: how close are weeks of on-chain price discovery to the true outcome? The honest answer depends entirely on which spot figures you compare, and the difference itself is the conclusion.

Compared to the truly crucial price—SpaceX's actual listing price—Perp was overpriced. It was about 30% higher than the IPO price of $135 and about 17% higher than the opening price of $150, and it remained listed for several weeks, not just minutes. Its real bet was on the intraday high: $176.52, almost exactly its own pre-market markup. So, to be fair, it's the opposite of the Cerebras case: Perp bet on the highest price, but not the opening price. It predicted where SpaceX wanted to go, but failed to predict at what price the record supply of new shares would be liquidated. Two points need clarification to avoid misattribution: the so-called "discount to within 1%" only holds true after the market opens, and half of it is mechanical: the ±10% boundary prevented the conversion drop at around $152, a point that appears accurate to the naked eye, but is actually due to the boundary's influence. Furthermore, maintaining a price close to the spot price after the introduction of real-time pricing is hardly a feat; any perpetual contract can do that. That's not something the market is trying to prove. What it's trying to prove is the prediction, which is about 17-30% overestimated.

Two things I'm carrying today

Ventuals' SPACEX contract was the first real-world test of its "settle-and-halt" mechanism. With SpaceX's IPO, the contract settled at the implied first-day closing valuation of $161.11, funding fees went to zero, and all positions were forcibly liquidated. This was the first real-world test of the endgame design described in §5.1: a market that dies on the listing day, rather than surviving through the listing process.

The stock split risk highlighted in §6.3 has now gone from an assumption to a real-time concern. trade.xyz's SPCX is now a perpetual stock held by a real-time external oracle, with no publicly disclosed rebase mechanism for the company's actions. An IPO is the safe event; the stock split, special dividend, or division after the first conversion is the one without any underlying mechanism to support it. SpaceX itself conducted a 5-for-1 stock split in May, which crippled Ventures' oracle, so whether high-priced stocks will split again is based on its own experience.

What should we be monitoring now?

Starting today, three things become measurable. First, funding costs finally have informational value. With IPO short selling scarce and expensive, Perp becomes the only cheap short-selling tool; and retail investors who can't get allocations and can only go long through FOMO can only enter Perp. The net direction of these two forces will be reflected in the funding costs for the first 30 days after the conversion. The data for the first three days is already out: Perp has converged back to the spot market, but it closed at approximately $172 on its first day of trading, a premium of about 7% over the Nasdaq closing price of $161; the funding costs after the conversion have remained slightly positive, increasing by about 0.005% every 8 hours (an annualized rate of about 5-6%), with long positions still paying a small holding fee. This "structural discount" scenario mentioned in the forecast hasn't appeared in the first three days. It's worth making this a permanent internal tracking indicator. Second, corporate action is an unresolved investment issue for this category. Whoever can provide a reliable on-chain rebase protocol, coupled with a redundant oracle oriented towards administrative facts, will fill the final gap, and this is precisely the area worth betting on (as such tools proliferate, so will perp-spot joint margin). Third, the after-hours story truly begins now. SpaceX's big news, whether launches or accidents, broke over the weekend, and the first weekend, when the Starship event triggered the world's only real-time price on Hyperliquid, was both the best time for event research and its best for dissemination in this category.

Conclusion: The price has been discovered, but the market is not yet complete.

Let's first discuss what this episode proves. Price discovery still works even without a spot market. A highly sophisticated oracle, operating perpetually solely through its own order book and a price range, kept Cerebras within 1.3% of its Nasdaq opening price, while SPCX, as its IPO approached, plummeted from the speculative upper limit of $216 to its IPO price of $135. It even did the same thing for crude oil over a weekend when all traditional markets were blacked out. The direction of information flow has quietly shifted.

Now let's look at the more difficult half of the scorecard. These venues excel at handling prices, but their event handling is still quite primitive. Market prices can beautifully digest continuous information, but company actions are not continuous information; rather, they represent an administrative change within an organization, and the on-chain technology stack simply lacks the means to process them. Trade.xyz lacks a rebase mechanism, so if a stock split actually occurs after the conversion, it will crash as a complete oracle, with funding fees unable to be corrected, and it won't even be aware of or able to stop the boundary when it's discovered.

Ventuals did create this "organ," but outsourced it to a single data provider. On May 28th, an expired split adjustment caused its flagship market to crash by 45%, liquidating holders who had correctly predicted everything except the pipeline. Even Binance, with its rebase mechanism, delayed implementation for ten days, resulting in the same company displaying two prices on two screens. Every operational failure in this report points to the same root cause: not that price discovery was flawed, but rather the lack of that tedious corporate action processing layer. Traditional markets spent a century standardizing it, yet no one found it interesting enough to warrant rebuilding it first.

This is also a fair way to score venue competition. Trade.xyz won not because its oracle was smarter. It won because its funding fee design made the trade almost cost-free to hold, because it launched on a catalyst rather than rushing to market, and because its pricing unit was integrated into the cross-venue arbitrage network. The same set of design choices that made it win was also the same set that exposed it: free holding meant an unanchored price, no rebase meant no solution for splits, and "convert and continue" meant inheriting the entire corporate action calendar of a listed company without any handling mechanism. Ventuals made the exact opposite trade-off: an anchor, taxes, and endgame death. It lost the volume war but was structurally immune to the kind of flaws that are still not priced in and lie dormant in the designs of its competitors.

This final warning is structural: these are essentially price trackers lacking an "event processing layer," and it's precisely this layer that makes a tracker worth holding with confidence. The real stress test for this category isn't the IPO itself, but the subsequent splits, special dividends, or spin-offs. Therefore, the opportunity is also specific: whoever can provide a credible, pre-announced corporate action mechanism on-chain, a publicly available rebase protocol, and a redundant oracle oriented towards administrative facts, will fill the final gap between these markets and the markets they are replacing. The price has been discovered; the market surrounding that price is still under construction.