Author: Chi Ann, Ryan Yoon, Tiger Research

This report, written by Tiger Research , analyses Ethereum’s dominance in the current real-world asset tokenization market, examines the structural challenges it faces, and explores which blockchain platforms are expected to lead the next phase of RWA growth.

Summary of key points

- Ethereum currently leads the RWA market with its first-mover advantage, past institutional experiments, deep on-chain liquidity, and decentralized architecture.

- However, general-purpose blockchains with faster and cheaper transactions, as well as RWA-specific chains designed to comply with regulatory requirements, are addressing Ethereum’s cost and performance limitations. These emerging platforms are positioning themselves as next-generation infrastructure by offering superior technical scalability or built-in compliance features.

- The next phase of RWA growth will be led by chains that successfully integrate three elements: on-chain regulatory compatibility, a service ecosystem built around real-world assets, and meaningful on-chain liquidity.

1. Where is the RWA market growing currently?

The tokenization of real-world assets (RWAs) has become one of the most prominent themes in the blockchain industry. Global consulting firms such as BCG have published extensive market forecasts, and Tiger Research has also conducted in-depth analysis of emerging markets such as Indonesia - highlighting the growing importance of this field.

So, what exactly is RWA? It refers to the conversion of physical assets such as real estate, bonds, and commodities into digital tokens. This tokenization process requires blockchain infrastructure. Currently, Ethereum is the main infrastructure supporting these transactions.

Source: rwa.xyz, Tiger Research

Despite growing competition, Ethereum has maintained its dominance in the RWA market. Dedicated RWA blockchains have emerged, and mature platforms in the DeFi space such as Solana are also expanding into the RWA space. Even so, Ethereum still accounts for more than 50% of total market activity, highlighting the solidity of its existing position.

This report examines the key factors that underpin Ethereum’s current dominance of the RWA market and explores the evolving conditions that are likely to shape the next phase of growth and competition.

2. Why can Ethereum maintain its leading position?

2.1. First-mover advantage and institutional trust

There are clear reasons why Ethereum has become the default platform for institutional tokenization. It was the first to introduce smart contracts and is actively preparing for the RWA market.

Backed by a highly active developer community, Ethereum established key tokenization standards such as ERC-1400 and ERC-3643 long before competing platforms emerged. This early foundation provided the necessary technical and regulatory foundation for pilot projects.

As a result, many institutions began evaluating Ethereum before considering alternatives. Several notable initiatives in the late 2010s helped validate Ethereum’s role in institutional finance:

JPMorgan Chase’s Quorum and JPM Coin (2016-2017): To support enterprise use cases, JPMorgan Chase developed Quorum, a permissioned fork of Ethereum. The launch of JPM Coin for interbank transfers demonstrated that Ethereum’s architecture — even in its private form — could meet regulatory requirements for data protection and compliance.

Societe Generale bond issuance (2019): SocGen FORGE issued a €100 million covered bond on the Ethereum public mainnet. This demonstrated that regulated securities can be issued and settled on a public blockchain while minimizing the involvement of intermediaries.

European Investment Bank Digital Bond (2021): The European Investment Bank (EIB) partnered with Goldman Sachs, Santander, and Societe Generale to issue a €100 million digital bond on Ethereum. The bond was settled using a central bank digital currency (CBDC) issued by the Banque de France, highlighting Ethereum’s potential in fully integrated capital markets.

These successful pilots reinforce Ethereum’s credibility. For institutions, trust is based on proven use cases and references from other regulated actors. Ethereum’s track record continues to attract attention, creating a reinforcing adoption cycle.

Source: Securitize

For example, in 2018, Securitize announced in an official document that it would build tools on Ethereum to manage the entire life cycle of digital securities. This move laid the foundation for the eventual launch of BlackRock's BUIDL fund, which is currently the largest tokenized fund issued on Ethereum.

2.2. Platform for real capital flow

Another key reason for Ethereum’s continued dominance in the RWA market is its ability to convert on-chain liquidity into real purchasing power. The tokenization of real-world assets is more than just a technical process. A fully functional market requires capital that can actively invest in and trade these assets. In this regard, Ethereum is the only platform with deep and deployable on-chain liquidity.

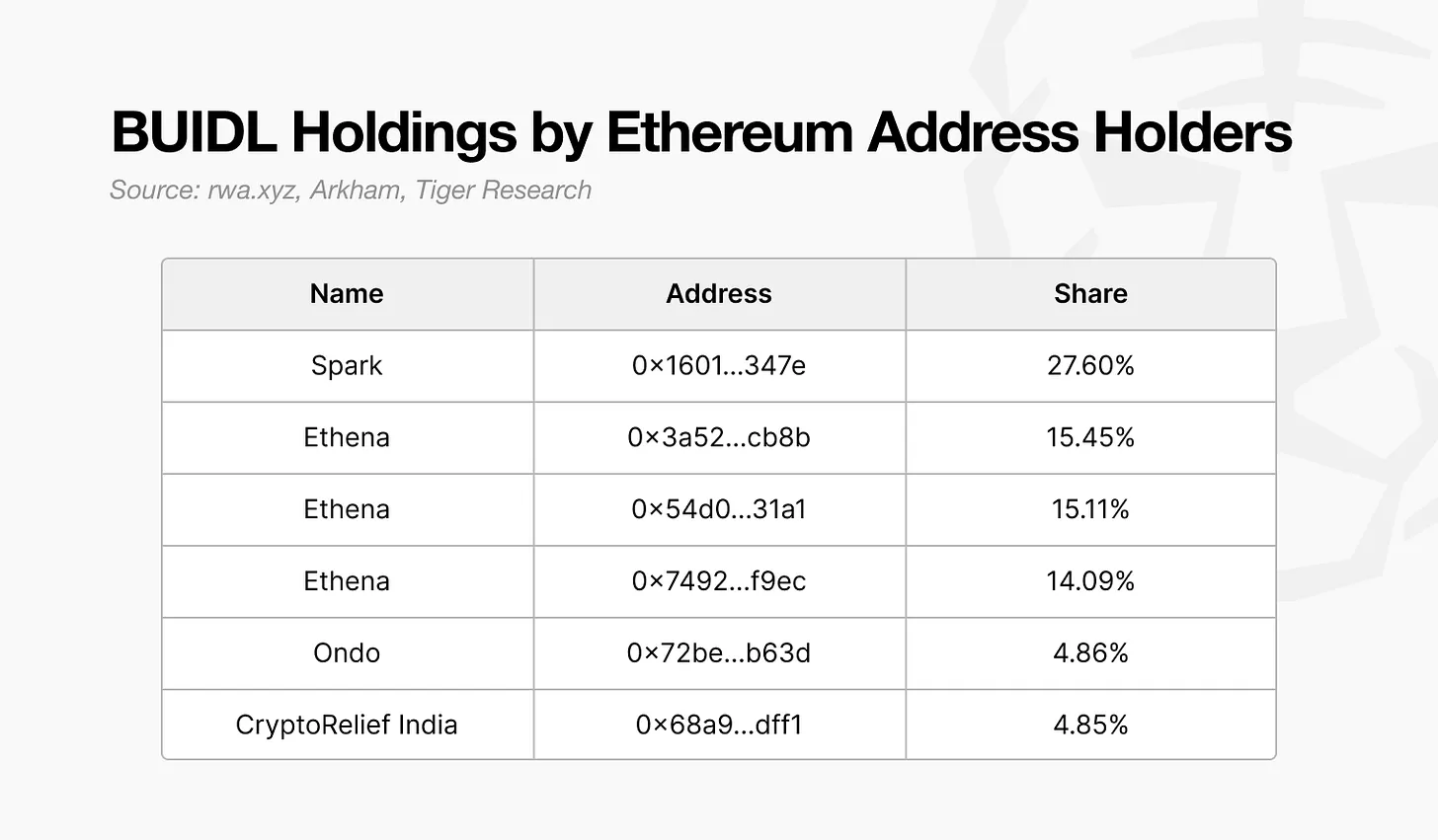

Source: rwa.xyz, Arkham, Tiger Research

This is evident in platforms like Ondo, Spark, and Ethena, all of which hold large tokenized BUIDL funds on Ethereum. These platforms have attracted hundreds of millions of dollars by offering products based on tokenized US Treasuries, stablecoin-based lending, and synthetic interest-bearing USD instruments.

Ondo Finance has amassed over $600 million in total value locked (TVL) through its treasury-backed products USDY and OUSG.

Spark Protocol leveraged DAI liquidity from MakerDAO to purchase over $2.4 billion worth of real-world Treasuries.

Ethena has built a bank-free yield infrastructure on Ethereum with its synthetic stablecoins USDe and sUSDe, attracting institutional demand and DeFi liquidity.

These examples show that Ethereum is more than just a platform for tokenizing assets. It provides a strong liquidity foundation that enables real investment and asset management. In contrast, many emerging RWA platforms have struggled to secure capital inflows or secondary market activity after the initial token issuance phase.

The reason for this difference is clear. Ethereum has integrated stablecoins, DeFi protocols, and compliance-ready infrastructure. This creates a comprehensive financial environment where issuance, trading, and settlement can all be done on-chain.

Ethereum is therefore the most efficient environment for converting tokenized assets into actual purchasing activity. This gives it a structural advantage beyond simple market share.

2.3. Building trust through decentralization

Decentralization plays a key role in building trust. Tokenization of real-world assets involves transferring ownership and transaction records of high-value assets to digital systems. In this process, the focus of institutions is on the reliability and transparency of the system. This is where Ethereum's decentralized architecture provides significant advantages.

Ethereum operates as a public blockchain, supported by thousands of independently run nodes around the world. The network is open to anyone, and changes are decided by consensus of participants rather than centralized control. As a result, it avoids single points of failure, ensures resilience to hacking and censorship, and maintains uninterrupted uptime.

In the RWA market, this structure creates tangible value. Transactions are recorded on an immutable ledger, reducing the risk of fraud. Smart contracts enable trustless transactions without intermediaries. Users can access services, execute agreements, and participate in financial activities without centralized approval.

These characteristics — transparency, security, and accessibility — make Ethereum a compelling choice for institutions exploring asset tokenization. Its decentralized system meets key requirements for operating in high-stakes financial environments.

3. Emerging challengers reshaping the landscape

The Ethereum mainnet has proven the viability of tokenized finance. However, along with its success, it has also exposed structural limitations that hinder broader institutional adoption. Key barriers include limited transaction throughput, latency issues, and unpredictable fee structures.

To address these challenges, Layer 2 Rollup solutions such as Arbitrum, Optimism, and Polygon zkEVM have emerged. Major upgrades including The Merge (2022), Dencun (2024), and the upcoming Pectra (2025) have brought improvements in scalability. Despite this, the network has not been able to match traditional financial infrastructure. For example, Visa processes more than 65,000 transactions per second, a level that Ethereum has not yet reached. For institutions that require high-frequency trading or real-time settlement, these performance gaps remain a key constraint.

Latency also presents challenges. Block generation takes an average of 12 seconds, and with the additional confirmations required for secure settlement, finality often takes up to three minutes. In cases of network congestion, this latency can increase further — creating difficulties for time-sensitive financial operations.

More importantly, gas fee volatility remains a concern. At its peak, transaction fees have exceeded $50, and even in normal times, costs often rise to over $20. This level of fee uncertainty complicates business planning and could undermine the competitiveness of Ethereum-based services.

Securitize illustrates this dynamic well. After running into the limitations of Ethereum, the company expanded to other platforms like Solana and Polygon, while also developing its own chain, Converage. While Ethereum played a crucial role in enabling early institutional experiments, it now faces increasing pressure to meet the needs of a more mature, performance-sensitive market.

3.1. The rise of fast, cost-effective, and universal blockchains

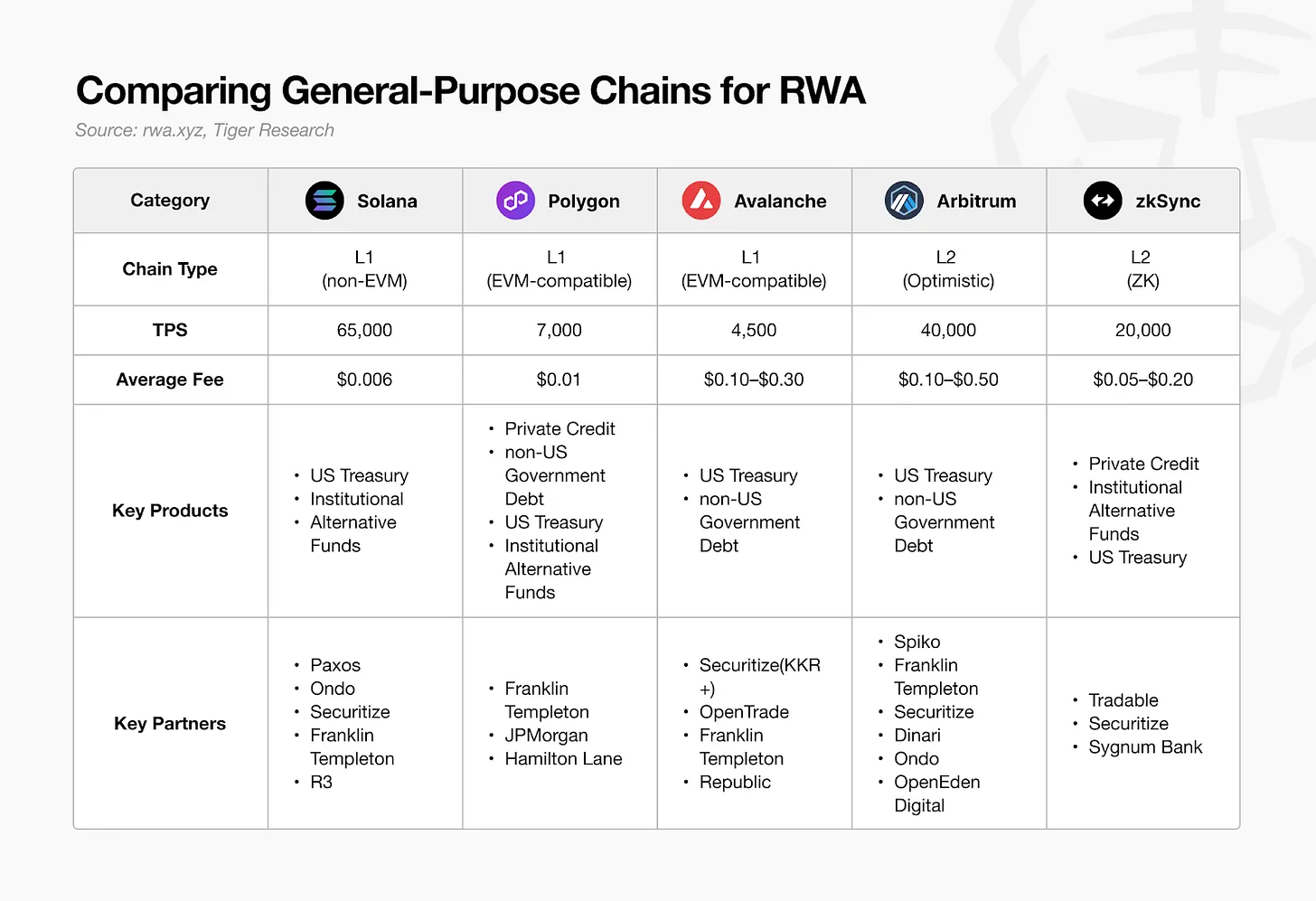

As Ethereum’s limitations become increasingly apparent, institutions are increasingly exploring alternative general-purpose blockchains that complement Ethereum by offering advantages around key performance bottlenecks such as transaction speed, fee stability, and finality time.

Source: rwa.xyz, Tiger Research

However, despite continued collaboration with institutional players, the actual number of tokenized assets on these platforms (excluding stablecoins) remains much lower compared to Ethereum. In many cases, tokenized assets launched on general-purpose chains are still part of a multi-chain deployment strategy led by Ethereum.

Even so, there are signs of real progress. In the private credit space, new tokenization initiatives are emerging. On zkSync, for example, the Tradable platform has gained traction, accounting for more than 18% of activity in the space — second only to Ethereum.

At this stage, general-purpose blockchains are just beginning to establish a foothold. Platforms like Solana, whose DeFi ecosystem has experienced rapid growth, now face a strategic question: how to convert this momentum into a sustainable position in the RWA space. Superior technical performance alone is not enough. To compete with Ethereum, it is necessary to provide infrastructure and services that can meet the trust and compliance expectations of institutional investors.

Ultimately, the success of these blockchains in the RWA market will depend less on raw throughput and more on their ability to deliver tangible value. The differentiated ecosystems built around each chain’s unique strengths will determine their long-term positioning in this emerging space.

3.2. The emergence of RWA-specific blockchain

More and more blockchain platforms are abandoning general-purpose designs in favor of specialization in specific areas. This trend is also evident in the RWA space, where a wave of new specialized chains built specifically for real-world asset tokenization optimization is emerging.

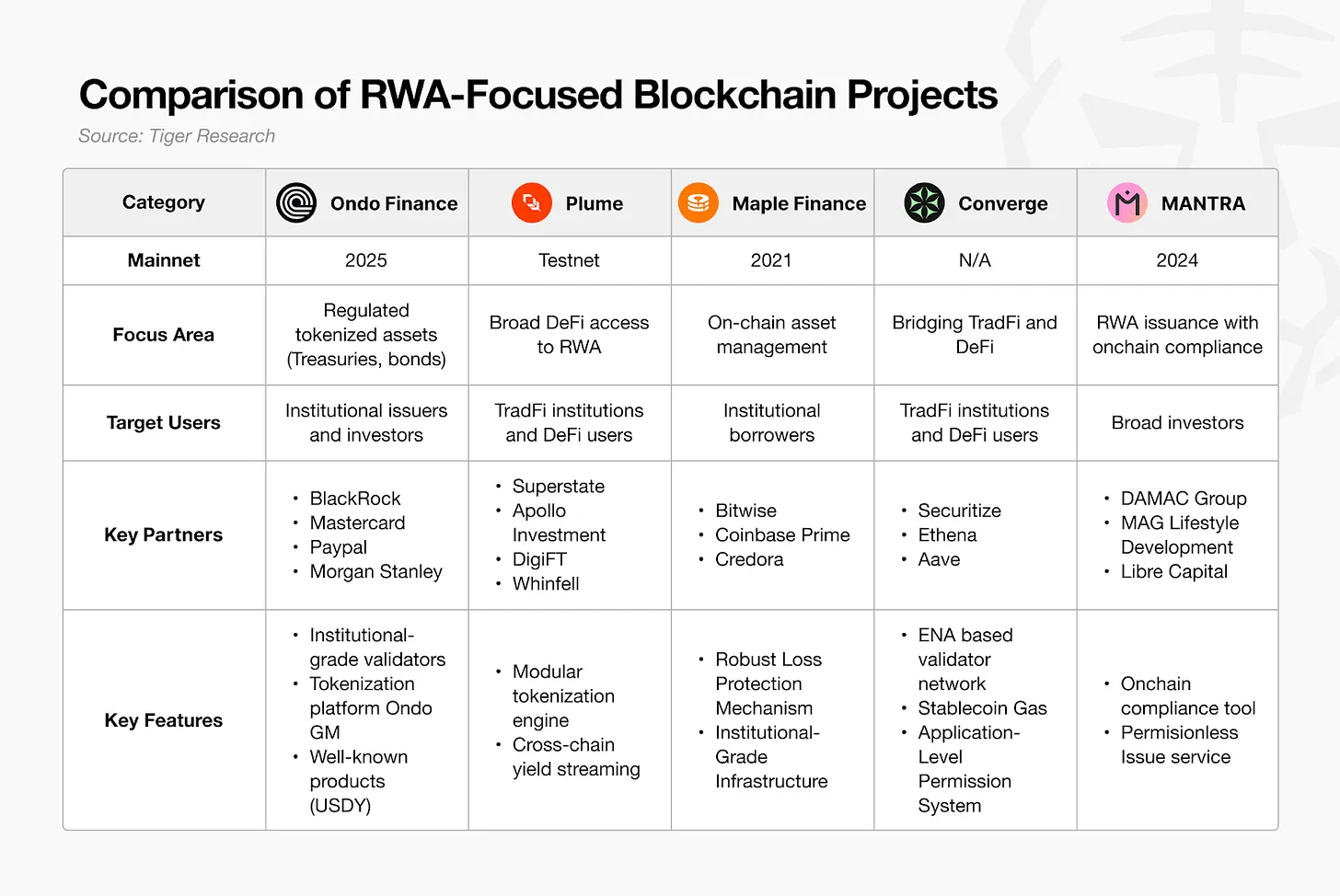

Source: Tiger Research

The case for a dedicated RWA blockchain is clear. The tokenization of real-world assets requires straightforward integration with existing financial regulations, which makes using general-purpose blockchain infrastructure inadequate in many cases. Specific technical requirements — especially around regulatory compliance — must be addressed from the ground up.

One key area is compliance processing. KYC and AML procedures are critical to the tokenization workflow, but these have traditionally been handled off-chain. This approach limits innovation because it simply wraps traditional financial assets in a blockchain format without redesigning the underlying compliance logic.

The shift now lies in moving these compliance functions entirely on-chain. Demand is growing for blockchain networks that are not only able to record ownership but also enforce regulatory requirements natively at the protocol layer.

In response, some RWA-focused chains have begun to offer on-chain compliance modules. For example, MANTRA includes decentralized identity (DID) functionality to support compliance enforcement at the infrastructure layer. Other dedicated chains are expected to follow a similar path.

In addition to compliance, many of these platforms use deep domain expertise to target specific asset classes. Maple Finance focuses on institutional lending and asset management, Centrifuge focuses on trade finance, and Polymesh focuses on regulated securities. Rather than broadly tokenizing widely held assets such as sovereign bonds or stablecoins, these chains use vertical specialization as a competitive strategy.

That being said, many of these platforms are still in their early stages. Some have yet to launch their mainnets, and most are still limited in terms of scale and adoption. If general-purpose chains are just beginning to gain traction in the RWA space, specialized chains are still at the starting line.

4. Who will lead the next phase?

Ethereum’s dominance of the RWA market is unlikely to continue in its current form. Today, the tokenized asset market is less than 2% of its projected potential, indicating that the industry is still in its early stages. Ethereum’s dominance to date stems primarily from its early discovery of product-market fit (PMF). However, as the market matures and scales, the competitive landscape is expected to change significantly.

Signs of this shift are already evident. Institutions are no longer focused on Ethereum alone. Both general-purpose and RWA-specific blockchains are being evaluated, and more and more services are exploring the deployment of custom chains. Tokenized assets, originally issued on Ethereum, are now expanding into a multi-chain ecosystem, breaking down the previous monopoly structure.

A key turning point will be the application of on-chain compliance. For blockchain-based finance to represent true innovation, regulatory processes such as KYC and AML must be conducted directly on-chain. If dedicated chains succeed in providing scalable, protocol-level compliance and driving widespread industry adoption, the current market landscape could be significantly disrupted.

Equally important is the existence of actual purchasing power. Tokenized assets only become investable when there is active capital willing to acquire them. Regardless of the technology, without meaningful liquidity, tokenization has limited utility. Therefore, the next generation of RWA platforms must foster a strong service ecosystem built on top of tokenized assets and ensure strong liquidity participation for users.

In short, the conditions for success are becoming increasingly clear. The next leading RWA platform is likely to be one that achieves the following three things:

A fully integrated on-chain compliance framework

A service ecosystem built on tokenized assets

Deep and sustainable liquidity to enable real investment

The RWA market is still in its infancy. Ethereum has proven the concept. The opportunity now lies with platforms that can provide better solutions - ones that meet institutional requirements while unlocking new value in the tokenized economy.