Author: Azuma , Odaily Planet Daily

The World Cup has begun, and the total trading volume of the prediction market is constantly hitting new highs, but Kalshi, as the industry leader, may not be in a good mood right now.

The reason was not the fluctuations in Kalshi's own business data, but because Kalshi suddenly faced another formidable rival after Polymarket, and this rival was once its most important ally.

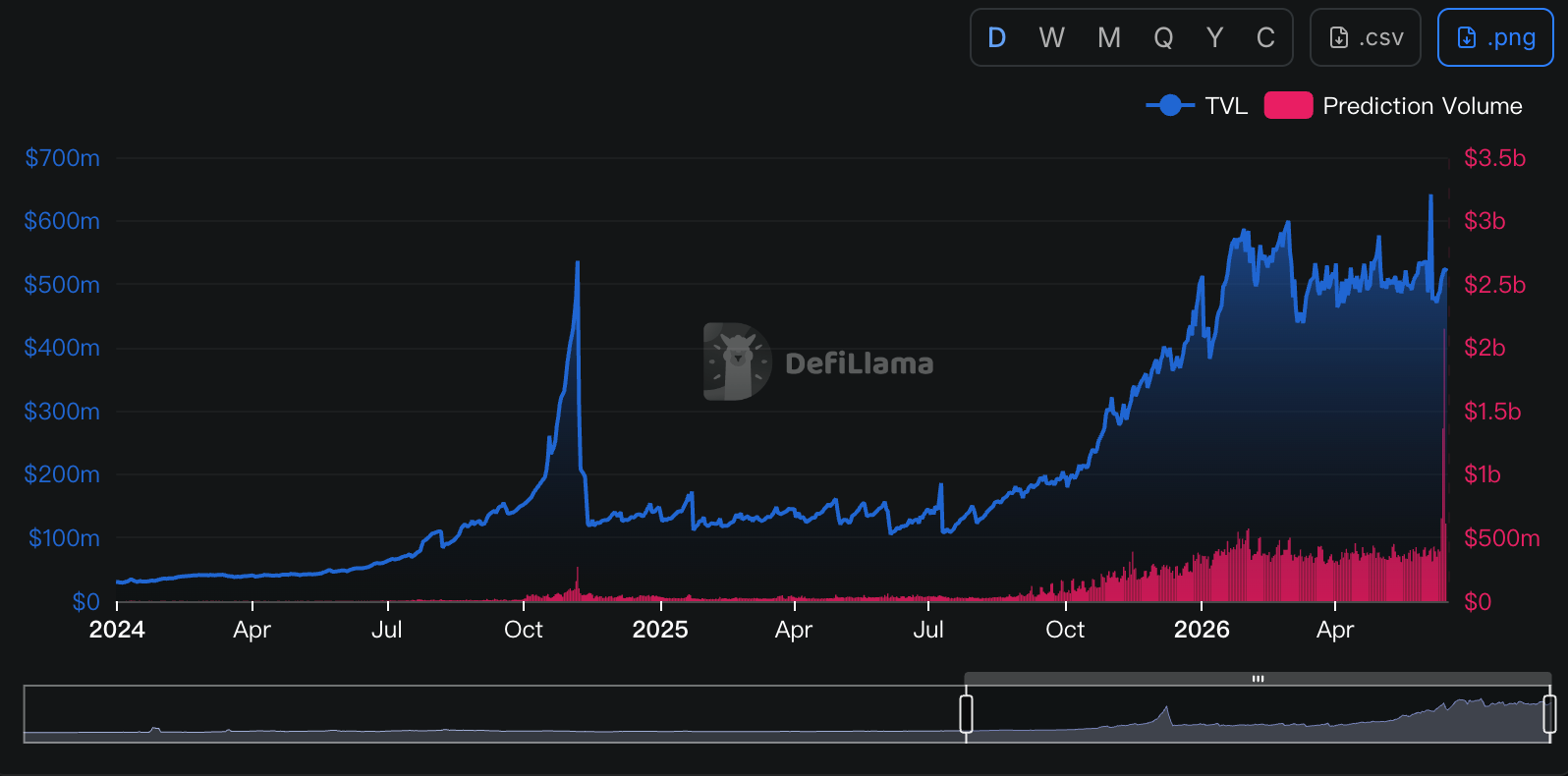

- Odaily Note: Data is taken from Defillama .

Kalshi's most important traffic channel - Robinhood

Let's rewind to March 2025. At that time, Kalshi announced a partnership with Robinhood, an American online brokerage firm, which would leverage Kalshi's resources to provide its users with prediction market trading services, allowing users to place bets on events related to politics, economics, and sports.

From a business model perspective, this is a typical "win-win" situation – Robinhood, responsible for user access and transaction distribution, can directly use Kalshi's mature products; while Kalshi, responsible for the underlying market, matching, clearing, and regulatory compliance system, can access Robinhood's huge pool of retail users.

Subsequent events proved the partnership to be a "win-win" situation. Through Robinhood's distribution channels, Kalshi indirectly gained a massive user base and transaction volume. Piper Sandler analysts estimated that "transactions completed through Robinhood accounted for approximately 25%-35% of Kalshi's total transaction volume." These orders ultimately translated into revenue for both parties—Robinhood would charge independently for all Kalshi event contracts traded through this channel, a fixed $0.01 per contract per direction, which was then shared with Kalshi (the specific percentage was not disclosed).

Robinhood's Q1 financial report, released at the end of April, showed that it completed 8.8 billion event contracts in Q1, driving "Other Transaction Revenue" up 320% year-over-year to $147 million. Prediction markets have become the fastest-growing new engine in Robinhood's product line.

But recently, this relationship has undergone some subtle changes.

Robinhood's ambition: to reclaim the cake that was given to Kalshi

As the history of the internet has proven countless times, once a channel gains enough influence, it will no longer be content with simply being a channel. Robinhood is no exception.

While the partnership with Kalshi has brought Robinhood considerable revenue, the company is no longer satisfied with its current revenue-sharing scheme as prediction markets have become one of the fastest-growing new businesses on the platform.

In their partnership, Kalshi initially provided the marketplace and infrastructure, while Robinhood provided the user base and order flow. However, as the collaboration deepened, Robinhood gradually realized that what was truly scarce might not be the marketplace itself, but rather the user entry point it firmly controlled. After all, for most Robinhood users, they didn't care whether the order was ultimately completed on Kalshi or another platform—users only saw a transaction entry point within the Robinhood App, not the underlying infrastructure provider.

In other words, Robinhood has always controlled one of the most important resources in the prediction market—distribution capabilities. Since the users belong to them, why should orders go to others?

In fact, while Robinhood was using Kalshi to quickly validate and predict market demand, another Plan B was launched shortly thereafter.

In November 2025, Robinhood announced a joint venture with Wall Street quantitative trading giant Susquehanna and plans to acquire MIAXdx, a CFTC-regulated derivatives exchange. According to official statements, the joint venture will operate an independent futures and derivatives exchange and clearinghouse, with prediction markets being one of its key areas of focus. At the time, it was largely seen as an infrastructure investment, but as more information was subsequently released, it became clear that Robinhood's goals went far beyond simply finding a new partner for prediction markets.

In January 2026, the transaction was officially completed. Robinhood and Susquehanna acquired 90% control of MIAXdx and took over a complete CFTC regulatory framework, including Designated Contract Market (DCM) and Derivatives Clearing Organization (DCO) accreditations. Subsequently, MIAXdx was renamed Rothera Exchange, and its clearinghouse was renamed Rothera Clearing.

At this point, Robinhood has all the core elements needed to independently operate a prediction market. All it lacks is a mature product that can rival Kalshi's, but for Robinhood, which has extensive experience in developing internet products, this is obviously not a difficult task.

Rothera's opportunity: the World Cup

In June 2026, after about six months of accelerated development, the Rothera product gradually took shape, and Robinhood finally made the move that was almost inevitable—to gradually transfer the orders that were originally going to Kalshi into its own control system.

Robinhood specifically chose an excellent launchpad for Rothera – the World Cup. In the prediction market, the World Cup is undoubtedly one of the most high-traffic trading themes. Whether it's match results, qualification outcomes, or the champion, related markets can attract a large number of new users to participate in trading in a short period. For Rothera, a newly launched platform, there is no better scenario for a cold start than the World Cup.

According to Robinhood's official disclosure, during the 104 matches of this World Cup, some event contracts will be routed to Rothera for matching and settlement, including market transactions related to single World Cup match results, the World Cup champion, and the total number of goals in a single match. Compared to the previous model that relied entirely on Kalshi, this is the first time Robinhood has imported prediction market orders into its own trading system on a large scale.

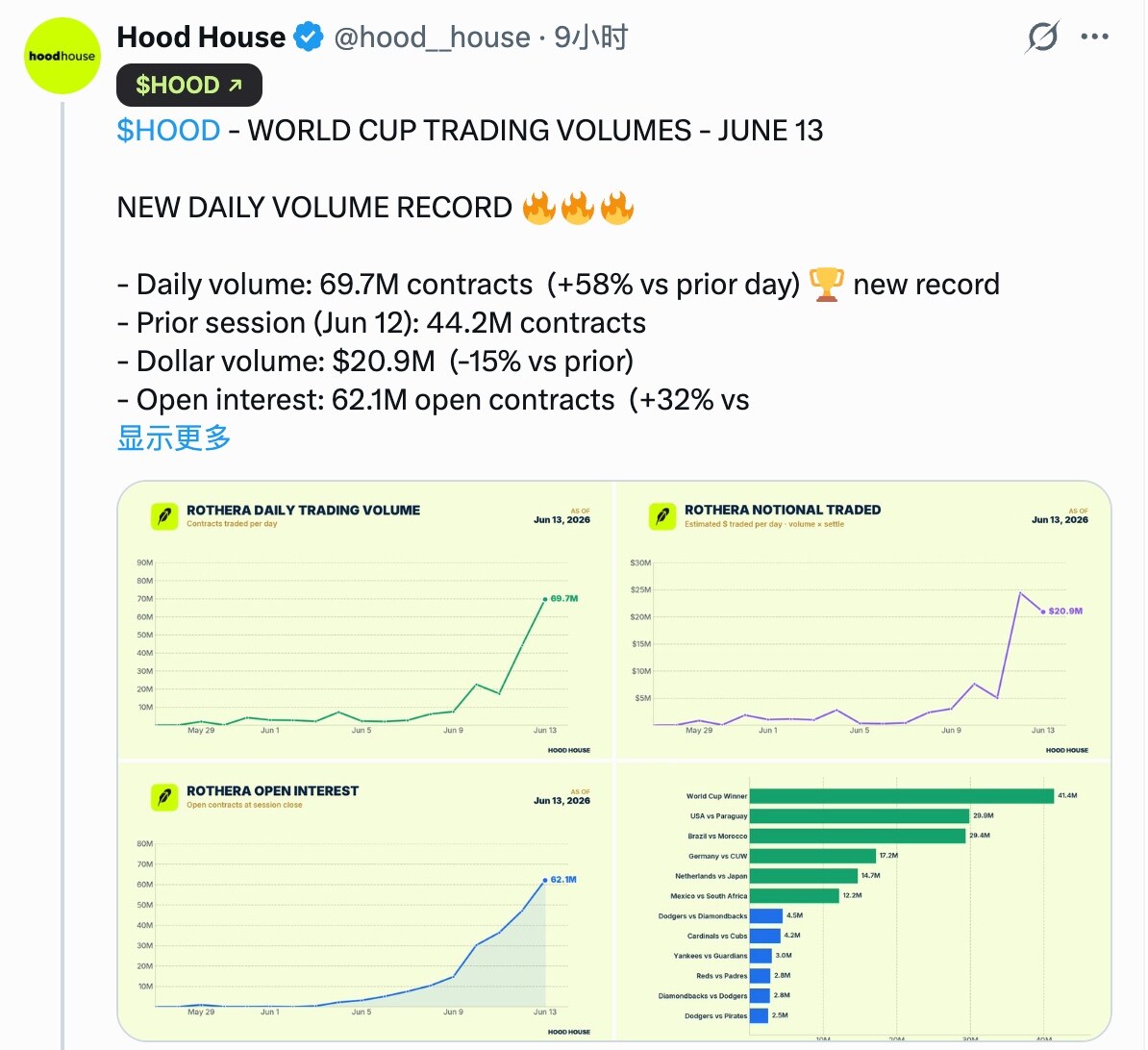

Judging from the results, Rothera clearly seized the opportunity. According to data disclosed by Hood House, an investment research media outlet that tracks Robinhood's activities, on June 12, Rothera completed 44.2 million contract transactions, corresponding to approximately $24.4 million in USD trading volume; on June 13, Rothera completed another 69.7 million contract transactions, corresponding to approximately $20.9 million in USD trading volume... Although these figures are still far from those of popular markets like Kalshi, which often involve hundreds of millions of dollars, considering that Rothera has only been online for a few days, this performance is already quite successful.

For Robinhood and Kalshi, this means the balance of their partnership has shifted. On Robinhood's side, transaction fee revenue that was previously shared with Kalshi can now remain largely within its own ecosystem; while on Kalshi's side, this signifies that one of its most important growth engines is beginning to show signs of weakening.

The World Cup is clearly just the beginning of Rothera's encroachment on Kalshi. Looking further into the future, Robinhood will inevitably expand Rothera's coverage to include more sporting events and economic and political topics, diverting orders that would otherwise go to Kalshi to Rothera.

Since Robinhood and Kalshi have never publicly disclosed their revenue-sharing ratio (reports suggest 50%:50, but no official information is available), we cannot know the exact value of this revenue siphon. However, considering that Robinhood generated $147 million in prediction market-related revenue in Q1 alone, and the World Cup in Q2 and the midterm elections further ahead could obviously bring even larger-scale transaction activity, this revenue siphon could be worth hundreds of millions of dollars on an annual basis.

Whoever controls the distribution controls everything.

The drama between Robinhood and Kalshi, from allies to rivals, once again illustrates a logic that has been repeatedly proven in the internet market: products are easy to create, but traffic is hard to find; whoever controls distribution controls everything.

In the past few years, the market has generally believed that Kalshi's core competitive advantages lie in its regulatory licenses, exchange qualifications, and clearing capabilities. Therefore, brokerages like Robinhood, as well as various media outlets, communities, and traffic platforms, are essentially just channels and traffic entry points for Kalshi. However, the emergence of Rothera proves one thing: in today's market saturated with similar products, the product itself may not be the most important factor. What is truly scarce is always the user base.

Where users are, liquidity is; where liquidity is, the market is. With access to tens of millions of retail users, Robinhood has the ability to direct those users to any trading venue. Users don't care whether their orders are ultimately executed on Kalshi or Rothera; as long as the experience is consistent, it doesn't matter who is facilitating and clearing the transactions.

If the theme of the prediction market industry in the past few years was the market battle between Polymarket and Kalshi, then the theme in the next few years may become a channel war. Robinhood's incubation of Rothera is essentially a reverse integration launched by the channel towards the market layer; and as more and more platforms with traffic entry points begin to realize the strategic value of prediction markets, similar stories are likely to continue to unfold. Whether it's exchanges, brokerages, social platforms, or media platforms, they could all become new entry points for prediction markets.

When entry points begin to control the market and channels begin to have pricing power, the ultimate winner in the prediction market industry may no longer be the platform responsible for matching orders, but the person closest to the user and with the greatest control over distribution.

This was true in the internet age, and it remains true in the mobile internet age. This time, there are no surprises.